Machine Learning

Shortcut to this page: ntrllog.netlify.app/ml

Notes provided by Professor Mohammad Pourhomayoun (CSULA)

Machine learning is using a set of algorithms that can detect and extract patterns from data to make predictions on future data. The process of detecting and extracting patterns from data is called training (this is the "learning" in "machine learning"). A machine learning model is trained so that the model can make predictions on future data. The data used to train the model is called the training data and the data used to make predictions is called the testing data.

There are many different types of machine learning algorithms and this page will explore how some of them work.

KNN (K-Nearest Neighbors): Like a near neighbor, State Farm is there. And there. And there.

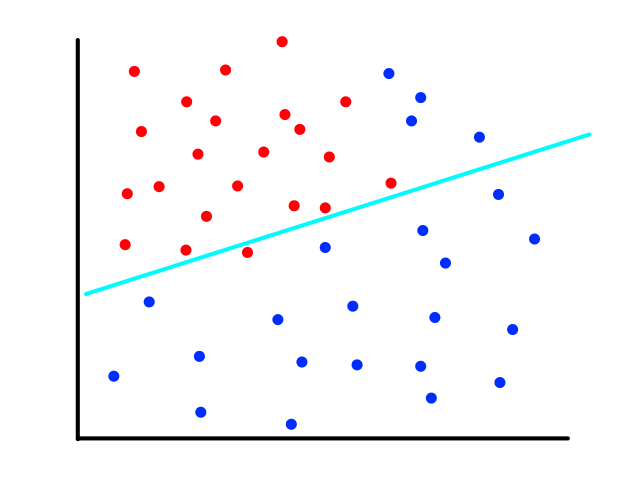

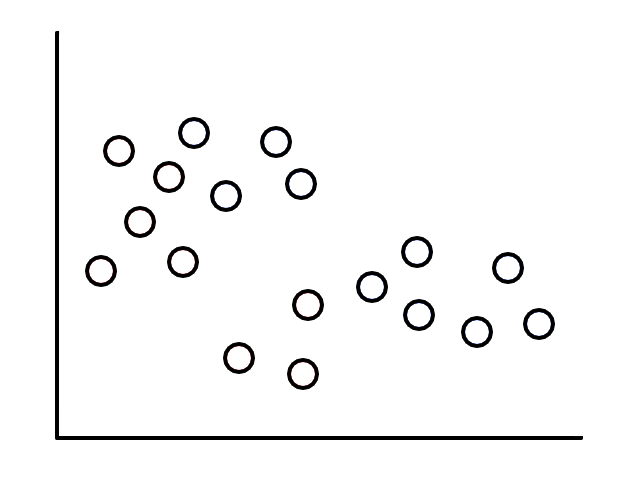

Let's say we took the time to scour a website and collect some weather data for Los Angeles.

| Humidity (%) | Temperature (°F) | Sunny/Rainy |

| 42 | 97 | Sunny |

| 43 | 84 | Sunny |

| 44 | 68 | Rainy |

| 94 | 54 | Rainy |

| 51 | 79 | Sunny |

| 91 | 61 | Rainy |

| 39 | 84 | Sunny |

| 47 | 95 | Sunny |

| 96 | 55 | Rainy |

| 90 | 84 | Rainy |

| Humidity (%) | Temperature (°F) | Sunny/Rainy |

| 60 | 84 | Sunny |

| 61 | 79 | Sunny |

| 61 | 68 | Rainy |

| 92 | 55 | Rainy |

| 26 | 77 | Sunny |

| 92 | 61 | Rainy |

| 54 | 81 | Sunny |

| 62 | 72 | Sunny |

| 94 | 61 | Rainy |

| 93 | 59 | Rainy |

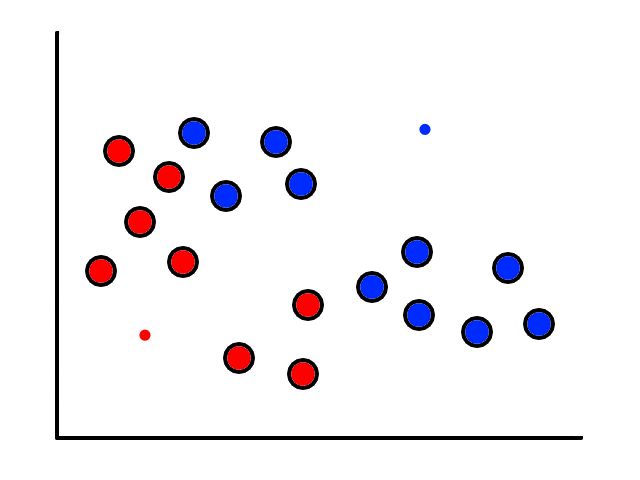

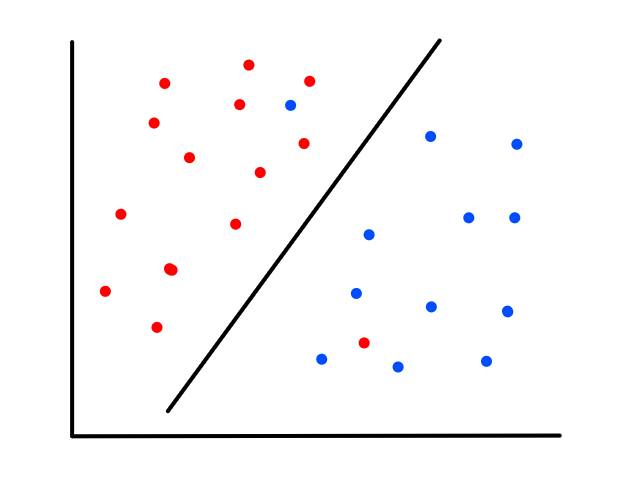

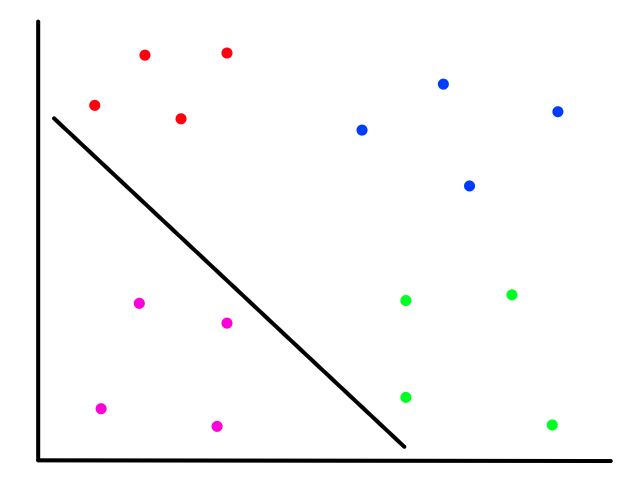

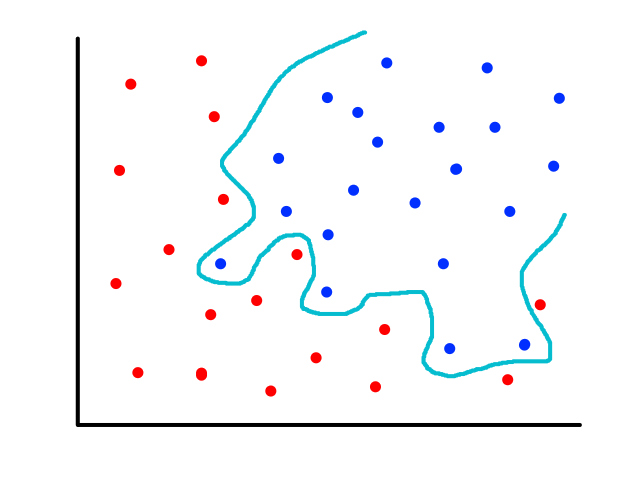

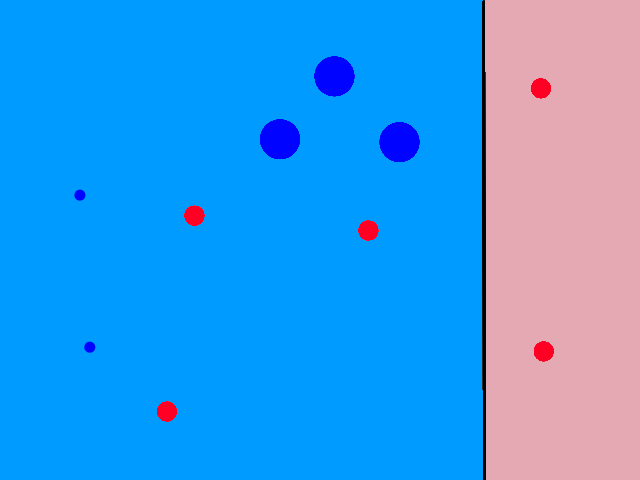

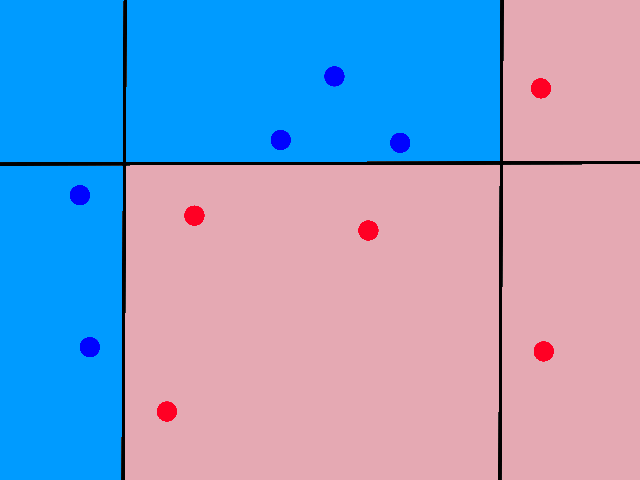

It's easy to notice that sunny days (red) are mostly in the top left and rainy days (blue) are mostly in the bottom right. Now let's say someone gives us the temperature (86°F) and humidity (59%) for a day and we have to guess whether it was rainy or sunny on that day (our lives depend on it!).

The temperature and humidity that the person gave us is plotted in green. Since it seems to be in red territory, we can guess that it was sunny on that day. 😎

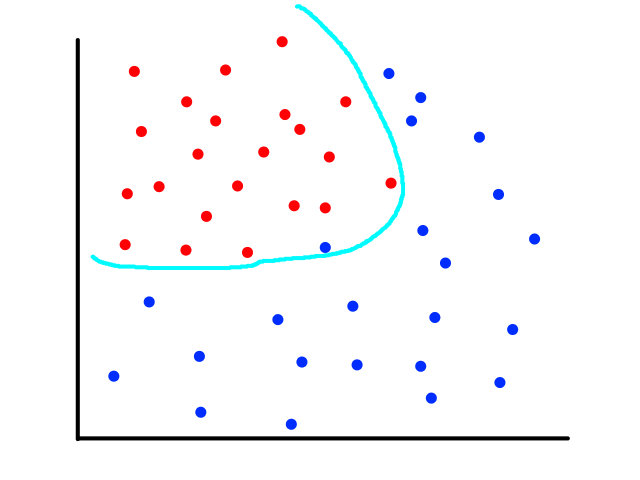

This is the basic idea behind KNN classification. For any point that we are trying to figure out, we look at the points that are closest to it (neighbors) to see what it is similar to. We assume that data points for a particular result share the same characteristics. For example, sunny days tend to have high temperatures and low humidity while rainy days tend to have low temperatures and high humidity.

This letter is short for the word "okay". What is K?

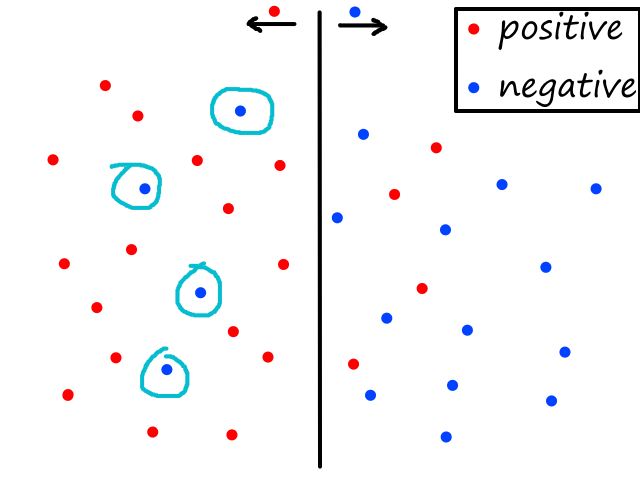

So looking at a point's neighbors allows us to make some guesses about that point. But how many neighbors do we need to look at, i.e., what should the value of `k` be?

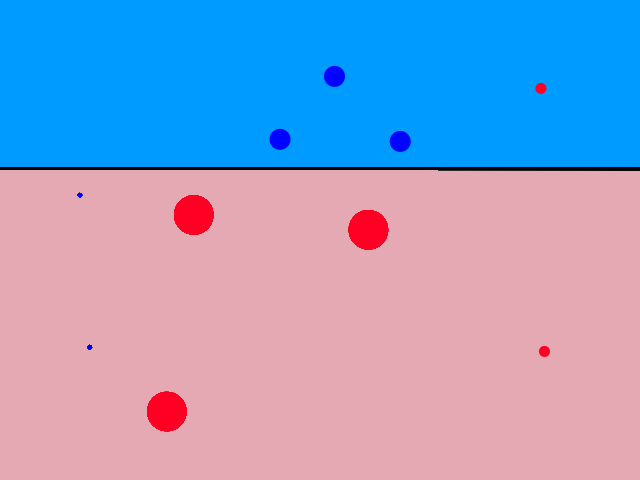

Using just 1 neighbor (`k=1`) is not a good idea.

The green data point is actually a sunny day, but let's pretend we didn't know whether it was rainy or sunny. If we looked at just 1 of its closest neighbors, we would think it was rainy. But if we look at, say, 5 of its closest neighbors, then the story changes.

It's now closer to more sunny days than rainy days, so we would then correctly guess that it was sunny.

Having more neighbors can also lessen the impact of outliers. For example, the left-most blue point (44% humidity, 68°F) could be considered an outlier since it is a rainy day with low humidity. But if we were to guess a random point in that general area (for example (40% humidity, 80°F)), it would be closer to more sunny days than rainy days so that outlier doesn't really affect the outcome.

Using more neighbors seems to be better since our decision is based on more information. So should we just use a ton of neighbors everytime?

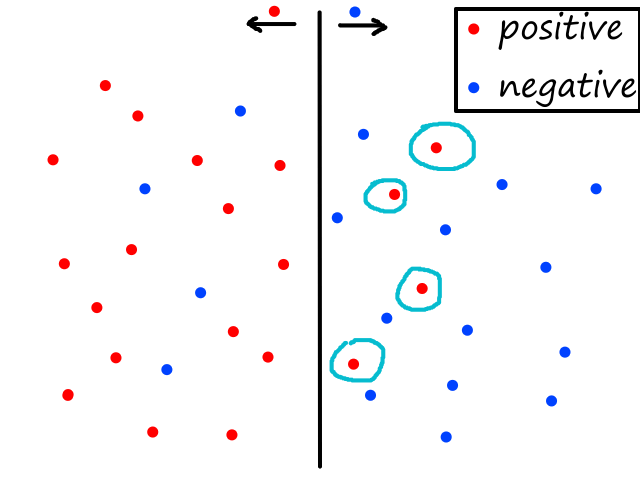

Let's suppose we only had information for 14 days instead of 20 and that significantly more of the days were sunny than rainy. The green point (80% humidity and 70°F) is unknown and we're trying to figure out whether it is rainy or sunny. Given its characteristics (low temperature and high humidity), it looks like it should be rainy.

Using 1, 2, 3, 4, or 5 neighbors, we do see that it is closer to more rainy days than sunny days.

However, look what happens when we start using more than 6 neighbors.

Now it is "closer" to more sunny days than rainy days. And it will stay this way even as we use more neighbors. This happened because the dataset was unbalanced (there were significantly more sunny days than rainy days in the dataset), so using more neighbors introduced a bias towards the more popular label.

So there is the possibility of using too few neighbors or too many neighbors. However, picking the right number of neighbors reliably is best done through trial and error.

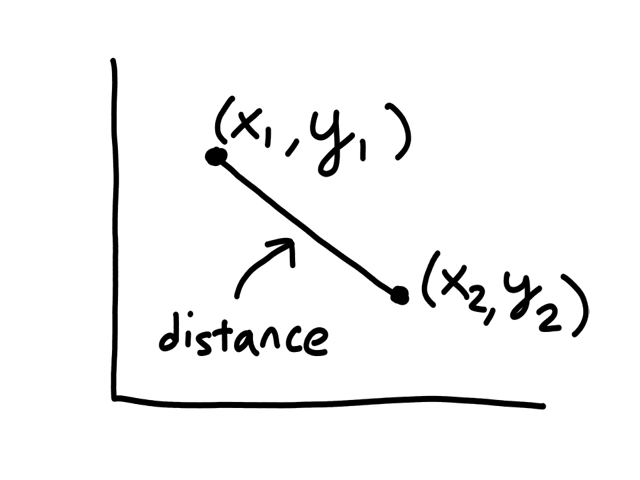

Euclidean Distance

So far, we have just been looking at the graph to see which points were neighbors to a given point. But computers can't "see" graphs, so they need to actually calculate the distance between each pair of points to see which of them has the shortest distance. (The points with the shortest distance to the given point are its neighbors.)

The formula for calculating the distance between 2 points `(x_1,y_1), (x_2,y_2)` is

`sqrt((x_1-x_2)^2+(y_1-y_2)^2)`

So to find the nearest neighbor of a given point, the computer has to calculate the distance between it and all the other points in the dataset. Then it sorts the distances to find the top `k` shortest distances. From this point of view, using a small number of neighbors makes things faster because there are less distances to calculate and sort.

Advantages of using a large `k`:

- ignores the effect of outliers

- better decision making

Advantages of using a small `k`:

- low computational complexity

- no bias towards popular labels

Normalization

A subtle thing to note about the weather data is that the scale of the units (percentage and degrees) was roughly similar. They both can theoretically range from 0-100. This is a good thing because there are some side effects of using units that aren't on a similar scale as each other.

To highlight this, we take a look at another dataset, which is completely made-up.

| Size (square feet) | Number of Bedrooms | Sold/Not Sold |

| 3000 | 1 | Sold |

| 4000 | 2 | Not Sold |

| 5000 | 3 | Sold |

| 6000 | 4 | Not Sold |

| 7000 | 5 | Not Sold |

The size of a house and the number of bedrooms it has are on completely different scales, with size in the thousands and number of bedrooms ranging from 1-5. So when we calculate distances between points, the number of bedrooms has a negligible impact on the distance. Consider this distance:

`sqrt((3000-4000)^2+(1-2)^2)`

`= sqrt((-1000)^2+(-1)^2)`

`= sqrt(1,000,000+1)`

and this distance:

`sqrt((3000-7000)^2+(1-5)^2)`

`= sqrt((-4000)^2+(-4)^2)`

`= sqrt(16,000,000+16)`

1,000,000 and 16,000,000 are really big numbers, so there's not much of a difference if we add 1 or 16 to them. This means that the effect of considering the number of bedrooms is practically negligible (we would get pretty much the same answer even if we didn't include the number of bedrooms in the calculation). It's like a millionaire finding a 20-dollar bill on the ground.

If the number of bedrooms is practically negligible, then KNN will — effectively — just look at the size of the house to predict whether or not it will be sold, which isn't what we want because we know the number of bedrooms should also have a significant impact. (🎵 Why you got a 12 car garage? 🎵) To prevent this, we can normalize the data so that the units are on the same scale.

One way to normalize data is to make the units on a scale from 0 to 1. We can do this by dividing each data point by the max value for that feature. In the housing dataset, the max size of a house is 7000 and the max number of bedrooms is 5, so we divide each size by 7000 and each number of bedrooms by 5.

| Size (square feet) [normalized] | Number of Bedrooms [normalized] | Sold/Not Sold |

| 0.4 | 0.2 | Sold |

| 0.6 | 0.4 | Not Sold |

| 0.7 | 0.6 | Sold |

| 0.9 | 0.8 | Not Sold |

| 1 | 1 | Not Sold |

The two distances calculated previously now become:

`sqrt((0.4-0.6)^2+(0.2-0.4)^2)`

`= sqrt((-0.2)^2+(-0.2)^2)`

`= sqrt(0.04+0.04)`

and:

`sqrt((0.4-1)^2+(0.2-1)^2)`

`= sqrt((-0.6)^2+(-0.8)^2)`

`= sqrt(0.36+0.64)`

Now the number of bedrooms has an impact on the distance.

Advantages and Disadvantages of KNN

Advantages of KNN:

- simple and requires low computational complexity

- all it's doing is calculating distances between points and then finding the shortest distances

Disadvantages of KNN:

- intensive when there are a lot of data points

- choosing a good `k` is hard

- most reliable way is through trial and error

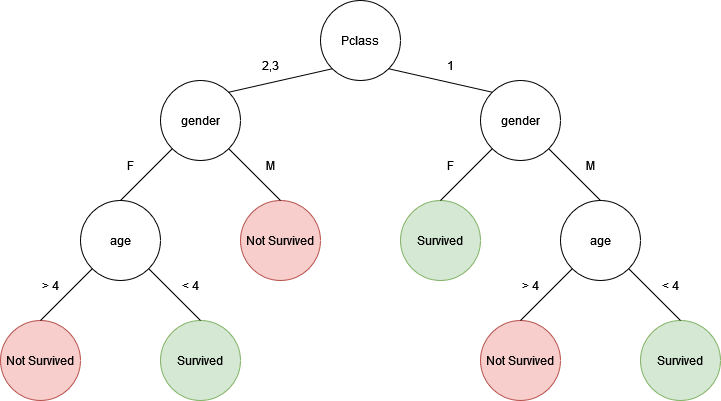

Decision Tree

Now we take a turn (but not into an iceberg) and look at people on the Titanic. Or at least 891 of them anyway. Green means the person survived and red means they didn't.

There are some negative ages, which means that the ages for those people are unknown.

There are some clear patterns in the data. For example, females had a higher survival chance than males did and younger (male) children had a higher survival chance than older (male) adults. #BirkenheadDrill. So if we chose a random person on the Titanic and tried to guess if they survived or not, a good start would be looking at age and gender. If they were female, they probably survived. If they were young, they probably survived. Of course, there were several males who survived and several older people who survived, but classifying based on gender and age is better than random guessing in this case.

We could also look at how fancy they were. The lower the number, the fancier. (🎵 We flyin' first class... 🎵)

There's also a clear pattern here. Higher-class passengers tended to survive while lower-class passengers didn't. So in addition to looking at age and gender, we could also use passenger class to predict whether a randomly-chosen person on the Titanic survived or not. #PayToWin. Also, the same age pattern kind of appears here, more so for class 2 and 3.

Another feature there is data for is how many parents or children each passenger was travelling with. So if someone has a value of 3, then they could've been travelling with their parents and child or their three children.

This time, there's not really a clear pattern. There's neither an increasing nor decreasing trend as we move between levels, i.e., the chance of survival for those travelling with 3 family members looks about the same as the chance of survival for those travelling with 2 or 1 family members. So looking at the number of family members someone was travelling with doesn't give us a good idea of survival chance.

So some useful features we found are age, gender, and passenger class, all of which we could use to predict whether someone survived or not. This could be represented using a tree, where first we check gender, then passenger class, then age.

Many things with this tree are arbitrary. Like which features to check and in what order. And what age to use as a threshold (e.g., 4). This tree is based on the manual visual analysis we did earlier, but how do we do this systematically (so that we can create a tree for any dataset) and reliably (so that the tree is actually able to predict correct results)?

First, we have to find out which features are important and which ones aren't. But what does "important" mean? In this case, a feature is important if it provides a good amount of information. For example, age, gender, and passenger class are important because they are all able to tell us whether a passenger survived. The number of family members is not important because it told us nothing about survival chance. But does age give us more information than gender? Or does gender give us more information than passenger class? We need a way to measure information.

Information Theory

There are two important concepts about information. The first is: the amount of information about an event has an inverse relationship to the probability of that event happening. This means that events that are likely to happen don't surprise us while events that don't happen often give us a lot of information. For example, "the sun will rise in the morning" doesn't give us a lot of information because we already know this will happen. However, "an eclipse will occur tomorrow" is news to us because it doesn't happen that often.

For an event `x`, the concept can be represented mathematically as

`I(x) prop 1/(p(x))`

where `I(x)` represents the amount of information of `x` and `p(x)` is the probability of `x` happening.

The second important concept about information is: when two independent events happen, the joint probability of them is the product of their probabilities and the total information about them is the sum of their information.

For example, there is a `1/2` chance of flipping a coin and getting heads and there is a `1/2` chance of flipping a coin and getting tails. So the probability of getting a head on the first flip and then a tail on the second flip is `1/2*1/2=1/4`. Getting a head and getting a tail are two independent events because the result of the coin flip does not depend on what happened in the past flips.

Let's say a coin is flipped twice, but we don't know the results of the two flips. If we ask about the first flip, then we get `1` piece of information. If we ask about the second flip, then we get another `1` piece of information. So then we would have `1+1=2` pieces of information.

Let `p_1` be the probability of one (independent) event happening and `p_2` be the probability of another (independent) event happening. Let `I` be a function that represents the amount of information learned from an event happening. Then the information from these two events happening (`I(p_1 cdot p_2)`) is the sum of their information (`I(p_1)+I(p_2)`).

`I(p_1 cdot p_2)=I(p_1)+I(p_2)`

So if there was a way to measure information, then it would have to turn products into sums. Luckily, the log function does just that.

Log properties:

- `log(x cdot y) = log(x) + log(y)`

- `log(1)=0`

- Notice that represents the information function quite nicely. If the probability of an event is `1`, then it gives us no information at all.

- `log(1/x)=-log(x)`

So a function that measures the information of an event should calculate the log of the probability of that event. Also, the amount of information about an event has an inverse relationship to the probability of that event happening (the first concept). Both of these lead to the formulation of the information function:

`I(x)=log(1/(p(x)))=-log(p(x))`

Entropy: "What is it?"

There's a term for the amount of information we don't know. Entropy. It measures the amount of "uncertainty" of an event. That is, if an event occurred, how certain can we be that we will know the results of that event? If we're not really sure what the outcome will be, then there is high entropy. If we're certain enough to bet money on the outcome, then there is low entropy.

Another interpretation of entropy is that it represents expected information. When an event has occurred, then we "expect" to receive some information from the result. This is why the formula for entropy (denoted as `H`) is the expected value (denoted as `E`) of the information:

`H(X) = E(I(X)) = sum_(x in chi) p(x) cdot I(x)`

`= -sum_(x in chi)p(x)log(p(x))`

where `chi` represents all the possible outcomes for event `X`

Typically entropy uses log base 2, in which case the unit of measurement is 'bits' (8 bits = 1 byte). When the entropy is measured in bits, the interpretation is that it takes that many bits to inform someone of the outcome. For example, an entropy of 0 means that no bits are required to convey information (because the probability of that event happening was 1 so we didn't need to make space to store that information). An entropy of 1 means that 1 bit is required to convey the outcome. In the case of a coin flip, heads can be encoded as 1 and tails can be encoded as 0. Either result would require 1 bit to store it.

1 is the maximum value for entropy though I have yet to have an explanation why.

If we have a fair coin (probability of heads is `1/2` and probability of tails is `1/2`) and an unfair coin (e.g., probability of heads is `7/10` and probability of tails is `3/10`), which coin is more predictable? Obviously, the unfair coin is more predictable since it is more likely to land on heads. We can prove this by calculating entropy.

There are only two possible outcomes for flipping a coin and the probabilities of those outcomes are both `1/2` for the fair coin. So the entropy of flipping a fair coin is

`-sum_(x in X)p(x)log_2(p(x))`

`= -(0.5log_2(0.5)+0.5log_2(0.5))`

`= 1`

The entropy of flipping the unfair coin is

`-sum_(x in X)p(x)log_2(p(x))`

`= -(0.7log_2(0.7)+0.3log_2(0.3))`

`~~ 0.88`

There is less entropy with flipping an unfair coin, which means there is less uncertainty with flipping an unfair coin. This makes sense because we know it is more likely to land on heads.

Also notice that there is an entropy of 1 when flipping a fair coin. This means that we are completely unsure of what the result will be, which makes sense because each result is equally likely.

Information Gain

If we gain information, then we reduce uncertainty. If we reduce entropy, then we gain information. Information gain is the measure of how much entropy is reduced.

And Now, Back to Our Regularly Scheduled Programming

Before the discussion on information theory, we needed a way to measure information so we could figure out which features of a dataset were important and which were more important than others so we could build a decision tree. Now we have a way to measure information — and lack thereof, a.k.a. entropy. So how do we use it to determine which features are important?

Let's go back to the titanic dataset and pretend that we knew nothing about it. We would have a hard time predicting survivability (again, forgetting everything that we just found out about the dataset). Now let's say we analyzed survivability by gender and found out that females were way more likely to survive than males. Now how hard would it be to predict survivability? Splitting the data by gender reduced uncertainty/entropy and increased information gain. So a feature is important if it reduces entropy.

This means that when deciding which features to put at the top of the decision tree (i.e., which features to check first), we should look for features that reduce entropy the most. If you were playing 20 questions, would you rather ask a question that provided you with more information or no information?

Feature Finding

Splitting the data by certain features can reduce entropy. The idea is that there is a certain amount of entropy before splitting the data, and after splitting the data, the entropy is lower. Some features will reduce the entropy more than others. To see this calculation in action, let's revisit the weather, but this time look at a different dataset.

| Temperature | Humidity | Windy | Label |

| high | low | yes | sunny |

| low | high | yes | rainy |

| high | low | no | sunny |

| high | high | yes | sunny |

| mild | mild | no | sunny |

| mild | high | no | rainy |

| low | mild | yes | rainy |

There are `7` samples, `4` of them are sunny and `3` of them are rainy. So the probability of a day being sunny is `4/7` and the probability of a day being rainy is `3/7`.

Calculating the entropy, we get:

`H(X) = -sum_(x in chi)p(x)log_2(p(x))`

`= -((4/7)log_2(4/7)+(3/7)log_2(3/7))`

`~~ 0.98`

Splitting the data on a feature means dividing the data into subsets based on that feature. For example, splitting the data on wind means putting all the windy data in one group and putting all the non-windy data in another group. This allows us to see how much of an impact that feature has on the result. So if we find out that the probability of a sunny day is high in the windy group and low in the non-windy group, then that means wind has an impact on whether a day is sunny or not. If the probability is pretty much the same in both groups, then that means wind does not affect whether a day is sunny or not.

🎵 It's gettin' windy here 🎵

Now let's try splitting the data on wind. There are `4` windy days with `1` of them being sunny and `3` of them being rainy. So if a day is windy, then the probability of that day being sunny is `1/4` and the probability of that day being rainy is `3/4`. Calculating the entropy for windy days, we get:

`H(X) = -sum_(x in chi)p(x)log_2(p(x))`

`= -((1/4)log_2(1/4)+(3/4)log_2(3/4))`

`~~ 0.81`

There are `3` non-windy days with `2` of them being sunny and `1` of them being rainy. So if a day is not windy, the probability of that day being sunny is `2/3` and the probability of that day being rainy is `1/3`. Calculating the entropy for non-windy days, we get:

`H(X) = -sum_(x in chi)p(x)log_2(p(x))`

`= -((2/3)log_2(2/3)+(1/3)log_2(1/3))`

`~~ 0.91`

We have two entropies for each of the values of the wind feature. Getting their weighted average will give us the average entropy after splitting the data on wind.

`E(H(X)) = sum_(x in chi)p(x)H(x)`

`= (4/7)(0.81)+(3/7)(0.91)`

`~~ 0.85`

So we went from an entropy of 0.98 to an entropy of 0.85 after splitting that data on wind. It's a slight decrease, but not by much. If we think about it, wind level generally doesn't tell us whether a day will be sunny or rainy.

🎵 It's gettin' humid here 🎵

Now let's try splitting the data on humidity. There are `3` high humid days with `0` of them being sunny and `3` of them being rainy. So if a day has high humidity, then the probability of that day being sunny is `0/3=0` and the probability of that day being rainy is `3/3=1`. Calculating the entropy for high humid days, we get:

`H(X) = -sum_(x in chi)p(x)log_2(p(x))`

`= -((0)log_2(0)+(1)log_2(1))`

`= 0`

At first glance, this may seem surprising. But looking at the dataset, every day with high humidity was rainy. So, according to this dataset, if a day has high humidity, it will always rain, so there is no uncertainty, hence the 0.

There are `2` mild humid days with `1` of them being sunny and `1` of them being rainy. So if a day has mild humidity, the probability of that day being sunny is `1/2` and the probability of that day being rainy is `1/2`. Calculating the entropy for mild humid days, we get:

`H(X) = -sum_(x in chi)p(x)log_2(p(x))`

`= -((1/2)log_2(1/2)+(1/2)log_2(1/2))`

`= 1`

Again, looking at the dataset, there was 1 mild humid sunny day and 1 mild humid rainy day. So if a day is mild humid, it can be either sunny or rainy. Maximum uncertainty.

There are `2` low humid days with `2` of them being sunny and `0` of them being rainy. So if a day has low humidity, the probability of that day being sunny is `2/2=1` and the probability of that day being rainy is `0/2=0`. Calculating the entropy for low humid days, we get:

`H(X) = -sum_(x in chi)p(x)log_2(p(x))`

`= -((1)log_2(1)+(0)log_2(0))`

`= 0`

Each time the day was low humid, it was sunny. So no uncertainty.

We have three entropies for each of the values of the humidity feature. Getting their weighted average will give us the average entropy after splitting the data on humidity.

`E(H(X)) = sum_(x in chi)p(x)H(x)`

`= (3/7)(0)+(2/7)(1)+(2/7)(0)`

`~~ 0.28`

This was actually a big decrease in entropy (from 0.98 to 0.28). This means that splitting the data on humidity reduces uncertainty by a lot, i.e., humidity gives us a lot of information about whether a day will sunny or rainy. We saw this with real data back in the KNN section.

🎵 It's gettin' hot in here 🎵

Now let's try splitting the data on temperature. There are `3` high temperature days with `2` of them being sunny and `1` of them being rainy. So if a day has high temperature, then the probability of that day being sunny is `2/3` and the probability of that day being rainy is `1/3`. Calculating the entropy for high temperature days, we get:

`H(X) = -sum_(x in chi)p(x)log_2(p(x))`

`= -((2/3)log_2(2/3)+(1/3)log_2(1/3))`

`~~ 0.91`

There are `2` mild temperature days with `1` of them being sunny and `1` of them being rainy. So if a day has mild temperature, the probability of that day being sunny is `1/2` and the probability of that day being rainy is `1/2`. Calculating the entropy for mild temperature days, we get:

`H(X) = -sum_(x in chi)p(x)log_2(p(x))`

`= -((1/2)log_2(1/2)+(1/2)log_2(1/2))`

`= 1`

There are `2` low temperature days with `0` of them being sunny and `2` of them being rainy. So if a day has low temperature, the probability of that day being sunny is `0/2=0` and the probability of that day being rainy is `2/2=1`. Calculating the entropy for low temperature days, we get:

`H(X) = -sum_(x in chi)p(x)log_2(p(x))`

`= -((0)log_2(0)+(1)log_2(1))`

`= 0`

We have three entropies for each of the values of the temperature feature. Getting their weighted average will give us the average entropy after splitting the data on temperature.

`E(H(X)) = sum_(x in chi)p(x)H(x)`

`= (3/7)(0.91)+(2/7)(1)+(2/7)(0)`

`~~ 0.67`

There was a big decrease (0.98 to 0.67), but not as big as the decrease from humidity. So temperature gives us a decent amount of information, but not as much as humidity. Which makes sense in real life because cold temperatures doesn't necessarily mean it's raining.

Top of the Tree

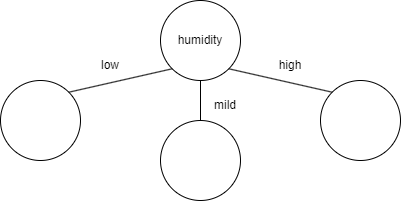

Humidity reduced entropy the most, so if we were building a decision tree to predict weather, the first feature to check would be humidity.

Temperature had the second most entropy reduction, but that doesn't mean it should be the next feature to check after humidity. That's because the calculation was entropy reduction from the starting entropy (0.98). After splitting the data, we're no longer working with the original dataset (because we've split the data). So if we were to continue building the tree after mild humidity, the new starting entropy would be 1 (calculated previously when it was gettin' humid in here) and we would be looking to see which feature (temperature or wind) would reduce that entropy value more. The same would have to be done for low and high humidity. In this case, the entropy for low and high humidity are both 0, so there's no reduction possible (which means based on this feature alone, we are able to tell whether a day is rainy or sunny). But theoretically, the branches below the second level of the tree could be different. For example, for low humidity, the best feature to check next might be temperature, but for mild humidity, the best feature to check next might be wind.

ID3 Algorithm

This is an algorithm to systematically build a decision tree. It's basically what we did above.

- Calculate entropy after splitting the data on every feature

- Select the feature that has the most entropy reduction

- Split the data into subsets using that feature and make a decision tree node for that feature

- Repeat with remaining features until

- no features left or

- all samples assigned to the same label (entropy is 0 for all nodes one level above all leaf nodes)

Viewer Discretization Is Advised

One thing that should be noted is that all the values for each feature were categorical values. They weren't numerical. For example, temperature was low, mild, high instead of 60, 75, 91. This is important because a decision tree shouldn't have branches for each numerical value. If the temperature is 90, then check this. If the temperature is 89, then check this. If the temperature is 88 ....

Let's say instead of low, mild, high for temperature, we had actual numerical values.

| Temperature | Humidity | Windy | Label |

| 90 | low | yes | sunny |

| 60 | high | yes | rainy |

| 92 | low | no | sunny |

| 89 | high | yes | sunny |

| 70 | mild | no | sunny |

| 73 | high | no | rainy |

| 61 | mild | yes | rainy |

Instead of building a decision tree for this dataset, we would want to first discretize the numerical values (i.e., convert the numbers into categories). Sorting the values first would help a lot.

| Temperature | Humidity | Windy | Label |

| 92 | low | no | sunny |

| 90 | low | yes | sunny |

| 89 | high | yes | sunny |

| 73 | high | no | rainy |

| 70 | mild | no | sunny |

| 61 | mild | yes | rainy |

| 60 | high | yes | rainy |

Now we need to define intervals/thresholds for what low, mild, and high temperatures are. Generally, the way to find the best threshold is to try every possible split to see which one minimizes entropy. However, there can sometimes be some more efficient ways to find the thresholds.

Looking at just temperature and label, we can notice that all days with temperature 89 and above are sunny and all days with temperature 61 and below are rainy. So we can decide that if a temperature is above 80, then it is considered high and if a temperature is below 65, then it is considered low.

Advantages and Disadvantages of Decision Tree

Advantages of Decision Tree:

- easily interpretable by a human

- it's easy to look at a tree and understand what it means and how to use it

- handles both numerical and categorical data

- (theoretically) works even with missing data*

- parametric algorithm

- just need to use training data once to build the tree, then use the tree to make predictions

- unlike KNN which needs to have the training dataset everytime to calculate distances for every prediction

- just need to use training data once to build the tree, then use the tree to make predictions

Disadvantages of Decision Tree:

- very prone to overfitting (see "A7) Overfitting")

- heuristic training techniques (brute force, trial and error)

- calculating entropy

- finding thresholds for discretizing numerical data

*Let's bring back the tree:

Will a 7-year old girl survive? Based on the tree, she will survive no matter what passenger class she is in. So even if there was no data for her passenger class, the tree could still (theoretically) make a prediction.

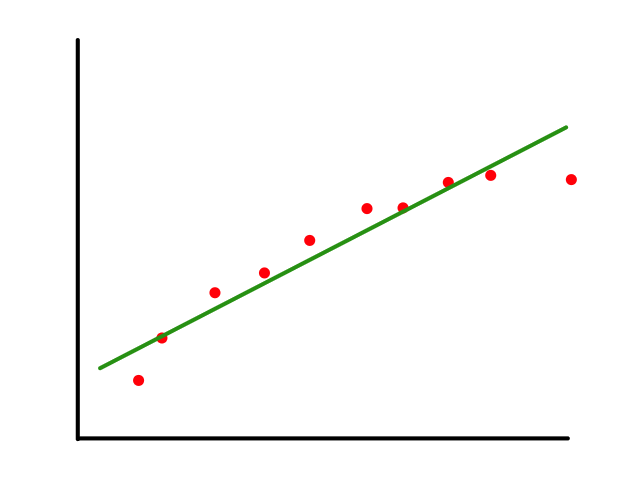

Linear Regression

So far, the algorithms we have looked at only predict categories, like sunny/rainy, sold/not sold, survived/didn't survive. But it is also possible to predict numerical values, like how much something will cost or how much rainfall an area will get.

To start, we can look at some fake data for housing prices. In this case, we are only looking at one feature (square footage) and the price that the house sold for.

We can predict the price of houses based on their square footage by drawing a line ("linear" regression) through the data points that best fits the data. So if there is a house with 2000 square feet, then we can predict that it will cost around $1,250,000.

Of course, the question now is how do we draw the line that "best fits the data" (and what does best fit mean exactly?)

Lining Them Up

The equation of a line is `y=ax+b`.

`a` is the slope and it controls how "rotated" the line is.

`b` is the y-intercept and it controls where the line is placed.

From here on, we will rename some stuff so that the equation of the line is

`y=ax+b`

`darr`

`h_theta(x)=theta_0+theta_1x`

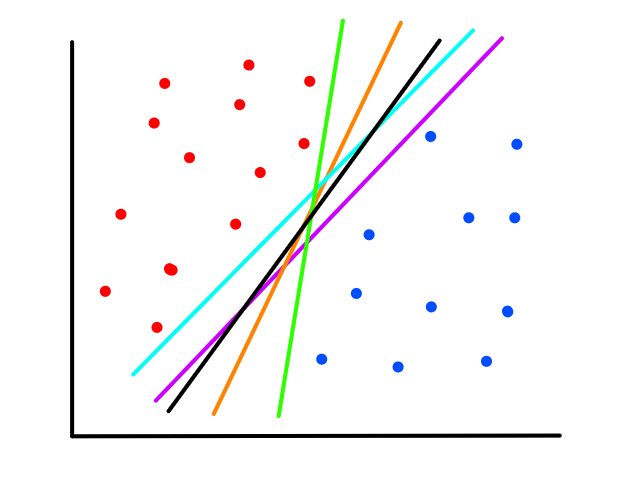

There are infinitely many possible lines that can be drawn.

So which line best fits the data?

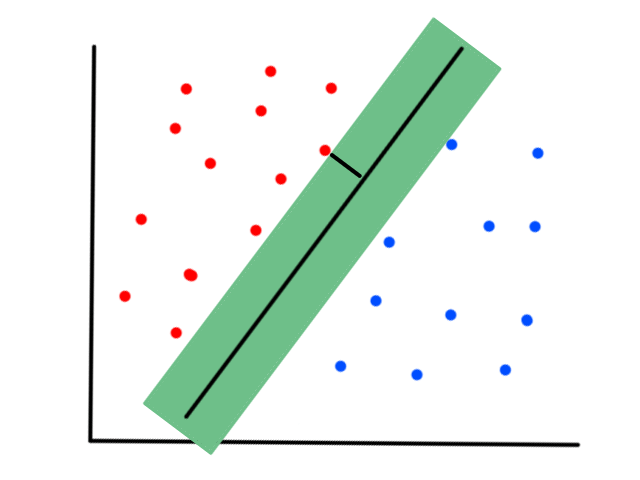

To create a line that will best fit the data points, we need to find values for `theta_0`, `theta_1` that will rotate and position the line so that it is as close as possible to all the data points.

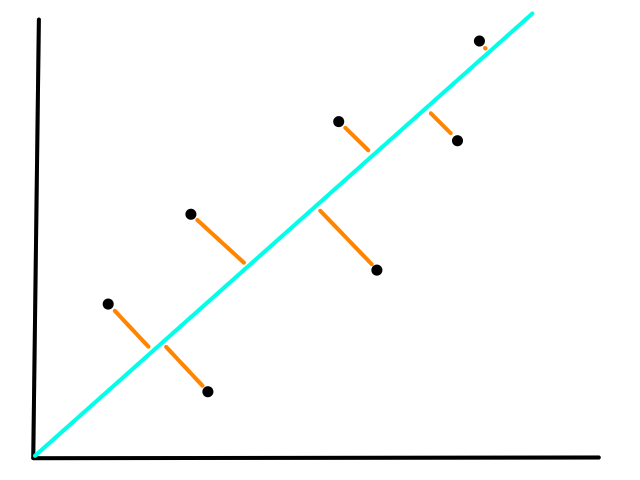

More formally, the line needs to minimize the differences between the actual data points and our predictions. In other words, we want to minimize the error between all of the actual values and all of our predicted values.

We are not minimizing error like what is shown below because we are only interested in minimizing error in the `y`-direction (not in the `x`- and `y`-direction). This is because the `y`-axis is the target value (what we are trying to predict).

So the idea is that for every line that we can draw, there is going to be some error for each data point. We can add up all those errors to get the total error for that line. So each line we can draw will have a total error. The line with the smallest total error is the best line.

Mathematically, we can define a cost function `J` that represents the total error:

`J(theta_0,theta_1)=1/(2m)sum_(i=1)^m(h_theta(x^((i)))-y^((i)))^2`

for `m` data points

(this is actually the total average error but it doesn't change things since it's still measuring amount of error)

- Why is there a power of `2`?

- The error between the actual value and the predicted value is `h_theta(x^((i)))-y^((i))`. This error can be negative if `h_theta(x^((i)))>y^((i))` (the predicted value is greater than the actual value), so we take the square of it to make it positive. We need positive values for errors so that we can get the total error.

- Another nice side effect is that lines that don't fit the data very well are "penalized" more than lines that do. This is because large errors squared affect the total error more than small errors squared do.

- Why not use absolute value to get positive errors?

- Minimizing a function involves taking the derivative of that function. So the function needs to be differentiable.

- What's with the `1/2`?

- When we take the derivative of that function, the `2`s will cancel out, so it is there to make things cleaner.

If we can find `theta_0`, `theta_1` such that `J(theta_0,theta_1)` is minimized (i.e., the total error is as small as possible), then we have found the values that will allow us to create the line `h_theta(x)=theta_0+theta_1x` that best fits the data.

Gradient Descent

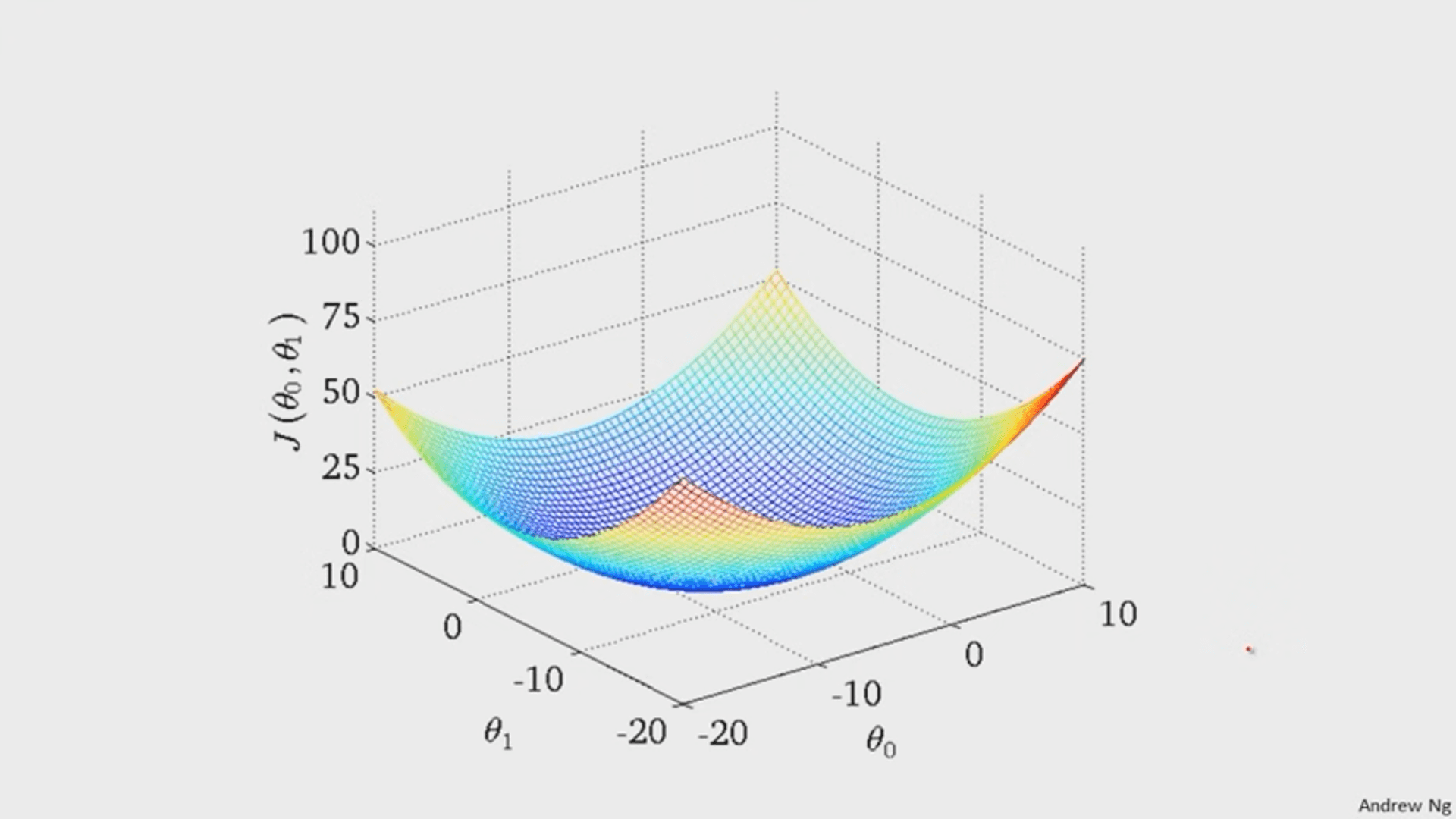

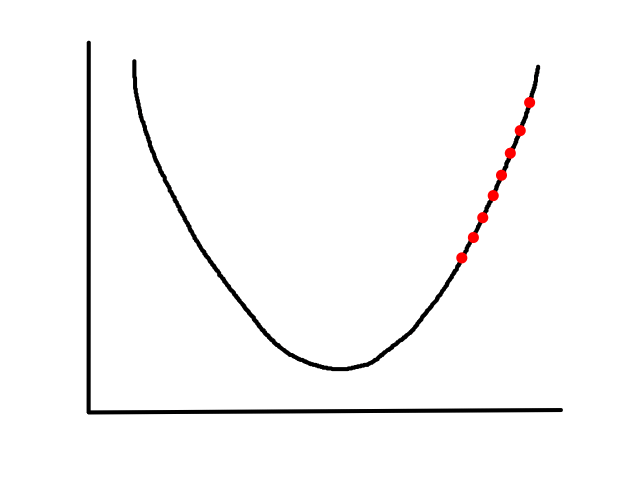

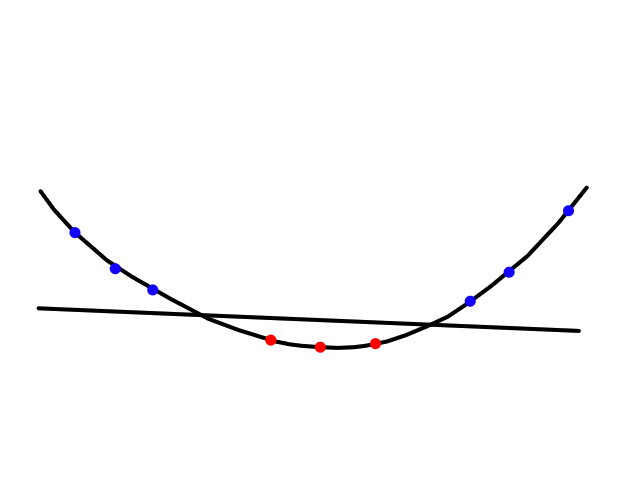

It turns out that the graph of the cost function is bowl shaped.

(image from Andrew Ng)

Since the cost function represents total (average) error, the bottommost point of the graph is where the total (average) error is smallest.

Whatever `theta_0` and `theta_1` are at that point are the values that create the line `h_theta(x)=theta_0+theta_1x` that best fits the data.

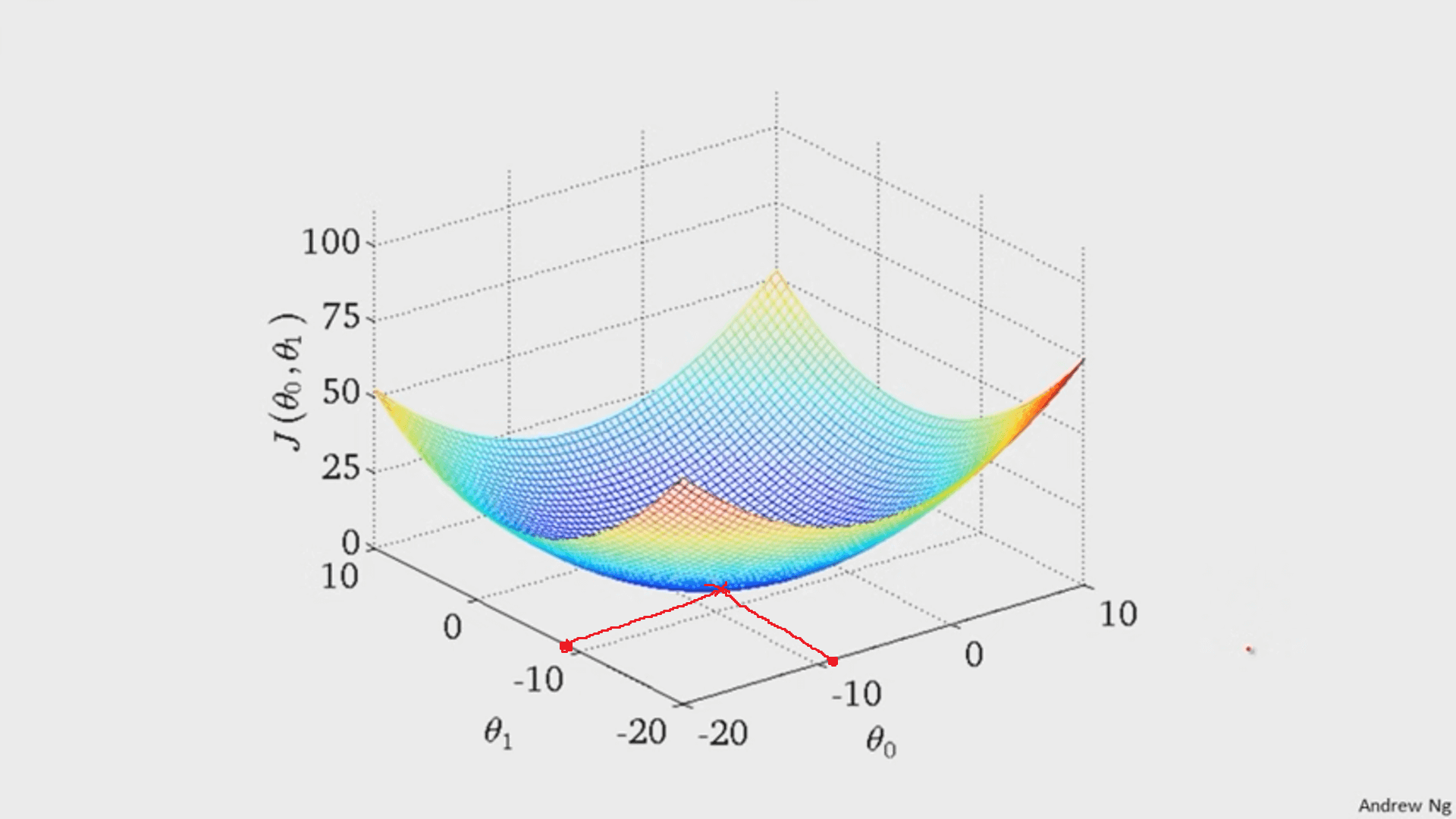

To find the minimum of `J(theta_0,theta_1)`, we have to perform gradient descent. The idea of gradient descent is that we start at a random point and take small steps towards the lowest point of the graph until we reach it.

So if we start at the dark blue point, the path it might take to get to the bottommost point might look like the above. And if we start at a different point, it could take a different path and reach a different point.

A gradient is the vector version of slope. Its magnitude is the slope (scalar value).

Mathematically, we find the vector that points in the most negative direction and take a step in that direction.

This is called the negative gradient, which points in the direction of the greatest rate of reduction. Taking a step in this direction is the fastest way in which the function decreases.

The gradient is a generalization of the concept of the derivative for functions of several variables.

Since the cost function is bowl shaped, there is only one minimum (the global minimum) so starting gradient descent at any point will always result in ending up at the same point (the minimum).

Starting at a random point `(theta_0, theta_1)`, taking a step means updating `theta_0` and `theta_1` by doing:

`theta_j = theta_j - alphadel/(deltheta_j)J(theta_0, theta_1)`

for `j=0,1`

Programmatically, there are two ways to implement this. The first way is to take both steps simultaneously:

`text(temp)0 = theta_0 - alphadel/(deltheta_0)J(theta_0, theta_1)`

`text(temp)1 = theta_1 - alphadel/(deltheta_1)J(theta_0, theta_1)`

`theta_0 = text(temp)0`

`theta_1 = text(temp)1`

The second way is to take one step at a time:

`text(temp)0 = theta_0 - alphadel/(deltheta_0)J(theta_0, theta_1)`

`theta_0 = text(temp)0`

`text(temp)1 = theta_1 - alphadel/(deltheta_1)J(theta_0, theta_1)`

`theta_1 = text(temp)1`

The first way is more efficient because it steps in the direction of `theta_0` and `theta_1` at the same time while the second way takes one step in `theta_0`, then in `theta_1`.

This is what it looks like from a 2D perspective.

Gradient descent starts from a random point and keeps moving down until it reaches the bottom. The bottom is where the slope is zero, so gradient descent will naturally stop (note how `theta_j`'s updated value is dependent on the slope). Each step naturally gets smaller as it moves further down because the slope gets smaller as it moves down (note how `theta_j`'s updated value is dependent on the slope).

`alpha` is called the learning rate, which controls how big of a step to take. Choosing a value that's too small will take a long time.

(no animation)

Choosing a value that's too big may result in overstepping the minimum. (And in some cases, it may diverge.)

So far we have the equation of a line that best fits the data:

`h_theta(x)=theta_0+theta_1x`

the cost function that represents the total (average) error of a line:

`J(theta_0,theta_1)=1/(2m)sum_(i=1)^m(h_theta(x^((i)))-y^((i)))^2`

and the formula for gradient descent:

`theta_j=theta_j-alphadel/(deltheta_j)J(theta_0,theta_1)`

After plugging everything in we get:

`theta_j=theta_j-alphadel/(deltheta_j)J(theta_0,theta_1)`

`=theta_j-alphadel/(deltheta_j)1/(2m)sum_(i=1)^m(h_theta(x^((i)))-y^((i)))^2`

`=theta_j-alphadel/(deltheta_j)1/(2m)sum_(i=1)^m(theta_0+theta_1x^((i))-y^((i)))^2`

`implies`

`theta_0=theta_0-alpha1/msum_(i=1)^mh_theta(x^((i)))-y^((i))`

`theta_1=theta_1-alpha1/msum_(i=1)^m(h_theta(x^((i)))-y^((i)))cdotx^((i))`

Basically, with gradient descent, we start at a random `theta_0` and `theta_1` and keep moving until we hit the minimum. The values of `theta_0` and `theta_1` at that minimum point are the values that create the line that best fits the data. From a line-drawing perspective, we start with a random line, see how good it is, then use the calculations to find a better line.

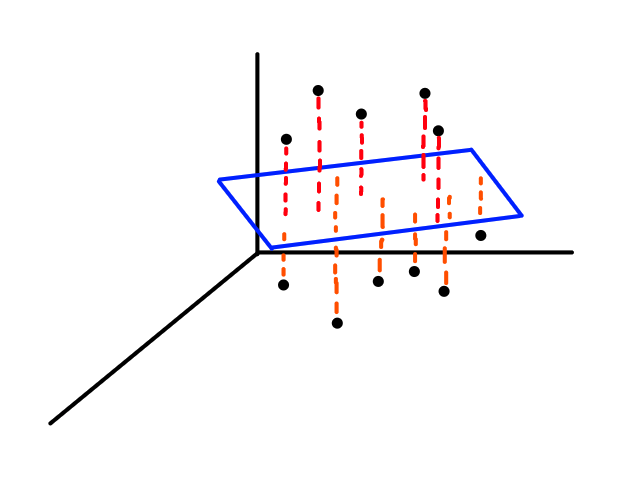

All of this is only for one feature though (that's why it's a line). To do linear regression with more than one feature, we need to extend the idea to higher dimensions.

Multiple Features

Let's say we had two features to look at: square footage and number of bedrooms.

| size in square feet | number of bedrooms | price |

| 1000 | 1 | 410,000 |

| 1200 | 2 | 600,000 |

| 1230 | 2 | 620,000 |

| 1340 | 3 | 645,000 |

If we were to graph this, it would be in 3D.

So the equation we would be looking for is:

`h_theta(bb x)=theta_0+theta_1x_1+theta_2x_2`

where `x_1` and `x_2` represent square footage and number of bedrooms

Instead of looking for the best line that fits the data, we would be looking for the best plane that fits the data.

As we work with more features, the object that best fits the data increases in dimensionality.

For `n` features, the equation of the object that best fits the data would be:

`h_theta(bb x)=theta_0+theta_1x_1+theta_2x_2+...+theta_nx_n`

We could define `bb x` to be a vector that contains the values for each feature:

`bb x=[[x_0],[x_1],[vdots],[x_n]]`

and `x_0=1`

and define `theta` to be a vector:

`bb theta=[[theta_0],[theta_1],[vdots],[theta_n]]`

so that the generalizable equation that best fits the data would be:

`h_theta(bb x)=bb theta^Tbb x`

The cost function is mostly the same:

`J(bb theta)=J(theta_0,theta_1,...,theta_n)=1/(2m)sum_(i=1)^m(h_theta(bb x^((i)))-y^((i)))^2`

and so is gradient descent:

`theta_j=theta_j-alpha1/msum_(i=1)^m(h_theta(bb x^((i)))-y^((i)))cdotx_j^((i))`

Notation: `bb x` (bold `x`) and `bb theta` (bold `theta`) are vectors.

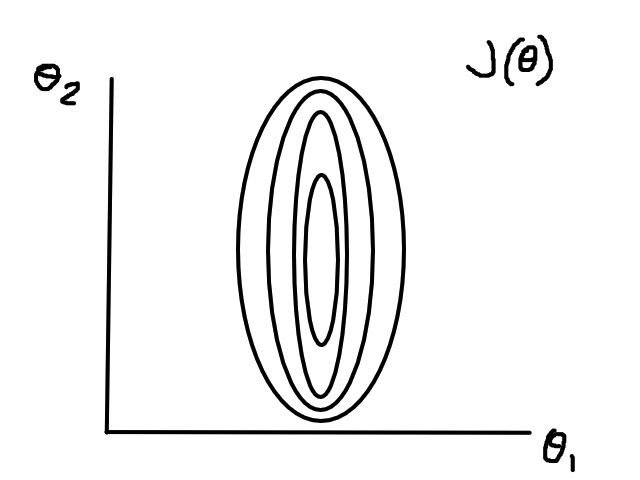

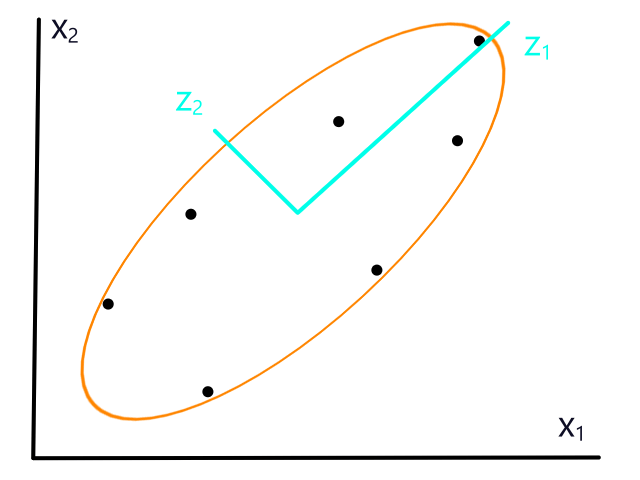

If the data isn't normalized, then gradient descent could take a long time. For example, if `theta_1` represented number of bedrooms and `theta_2` represented square footage, then the (contour) graph of the cost function could look like this:

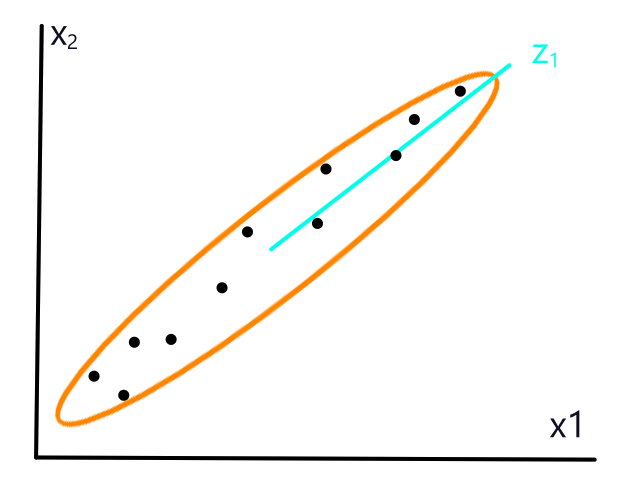

Normalizing would make the (contour) graph of the cost function more circular.

Logistic Regression

Although linear regression is used to predict continuous values, the ideas behind it can be used to build a classifier. Logistic regression is a classification technique that uses linear regression.

Let's say we had data where the labels can only be 0 or 1. For example, the `x`-axis could be tumor size and the `y`-axis could be whether or not the tumor is malignant (1 means yes and 0 means no).

We could theoretically draw a line that best fits the data like so:

However, since the output can only be 0 (not malignant) or 1 (malignant), the values on the line below `y=0` and above `y=1` are not relevant. For example, if the tumor size is 14, the output is 2. But what does 2 mean? In this simple example, we're assuming that large tumors are malignant, so we would want a size 14 tumor to output to 1 somehow. So we need something other than a straight line for this.

Sigmoid Function

Fortunately, there is a function called the sigmoid function that takes in any input and outputs a value between 0 and 1.

`g(z)=1/(1+e^(-z))`

As `z` moves towards `oo`, the function approaches `1` (since `e^(-z)` approaches `0`). As `z` moves towards `-oo`, the function approaches `0` (since `e^(-z)` approaches `oo`).

We can apply the sigmoid function to our line to effectively transform our line to a curve.

`h_theta(bb x)=bb theta^T bb x`

`g(z)=1/(1+e^(-z))`

`implies`

`g(bb theta^T bb x)=1/(1+e^(-bb theta^T bb x)`

This is what the graph looks like when we apply the sigmoid function to the line that best fit the tumor data:

(It looks like a straight line, but I promise it's "sigmoidy".)

The line that best fit the tumor data was `h_theta(x)=1/6x-1/3`. Applying the sigmoid function to that line, we get:

`g(1/6x-1/3)=1/(1+e^(-(1/6x-1/3)))`

So after applying the sigmoid function to `h_theta`, the new `h_theta` will only output values between 0 and 1. The values should be interpreted as probabilities that inputs will have an output of 1 (e.g., `h_theta(x)=0.7` means that `x` has a 70% chance of being 1). Since we're building a classifier, we should define a threshold to convert those probabilities into categories. For example, if an input has a probability greater than 0.5, then we can classify it as 1.

The threshold doesn't have to be fixed at 0.5. It can change depending on the situation. If we're predicting earthquakes, we want to minimize false alarms, so the threshold should be pretty high (e.g., greater than 0.8). We can reduce the threshold to make the model more sensitive or increase the threshold to make it less sensitive.

All of This for Nothing?!

This process of training a linear regression model, applying the sigmoid function to it, and then discretizing the output is generally not a good idea though as it can lead to poor results since the line that best fits the data (and thus the curve generated from that line) won't generally fit the data well to begin with.

So instead of turning a line into a curve, we should just make a good curve. The setup is still the same:

`h_theta(x)=g(bb theta^T bb x)=1/(1+e^(-bb theta^T bb x))`

where `bb theta=[[theta_0],[theta_1],[vdots],[theta_n]]` and `bb x=[[x_0],[x_1],[vdots],[x_n]]`

To make the curve, we need to find the values of `bb theta`. And just like in linear regression, to find the values of `bb theta`, we need gradient descent!

A New Cost Function

We also need a new cost function. The cost function from before was:

`J(bb theta)=J(theta_0,theta_1,...,theta_n)=1/(2m)sum_(i=1)^m(h_theta(bb x^((i)))-y^((i)))^2`

Before, `h_theta(bb x^((i)))` was linear, so the cost function was a convex bowl. Now, `h_theta(bb x^((i)))` is not linear anymore since we're applying the sigmoid function to it. As a result, the cost function looks something like this:

It is not guaranteed that starting at any point will converge to the global minimum (it might hit one of the other local minimums instead). This is why we need a new cost function, which actually turns out to be:

`J(bb theta)=J(theta_0,theta_1,...,theta_n)=-1/msum_(i=1)^m[y^((i))logh_theta(bb x^((i)))+(1-y^((i)))log(1-h_theta(bb x^((i))))]`

Gradient descent stays the same:

`theta_j=theta_j-alpha1/msum_(i=1)^m(h_theta(bb x^((i)))-y^((i)))cdotx_j^((i))`

Why does this cost function work?

Let's suppose for a single data point, `y=1`. Then the cost function will be:

`-[y^((i))logh_theta(bb x^((i)))+(1-y^((i)))log(1-h_theta(bb x^((i))))]`

`=-[1*logh_theta(bb x^((i)))+(1-1)log(1-h_theta(bb x^((i))))]`

`=-logh_theta(bb x^((i)))`

and the graph of it will look something like:

If we also predicted 1 (i.e., `h_theta(bb x^((i)))=1`), then the cost/error is 0 (i.e., `J(bb theta)=0`). But if we predicted 0, then the cost/error is infinite.

Now let's suppose for a single data point, `y=0`. Then the cost function will be:

`-[y^((i))logh_theta(bb x^((i)))+(1-y^((i)))log(1-h_theta(bb x^((i))))]`

`=-[0*logh_theta(bb x^((i)))+(1-0)log(1-h_theta(bb x^((i))))]`

`=-log(1-h_theta(bb x^((i))))`

and the graph of it will look something like:

If we also predicted 0 (i.e., `h_theta(bb x^((i)))=0`), then the cost/error is 0 (i.e., `J(bb theta)=0`). But if we predicted 1, then the cost/error is infinite.

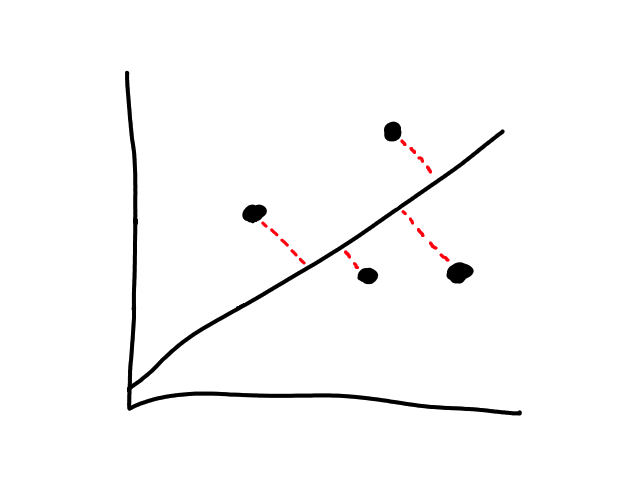

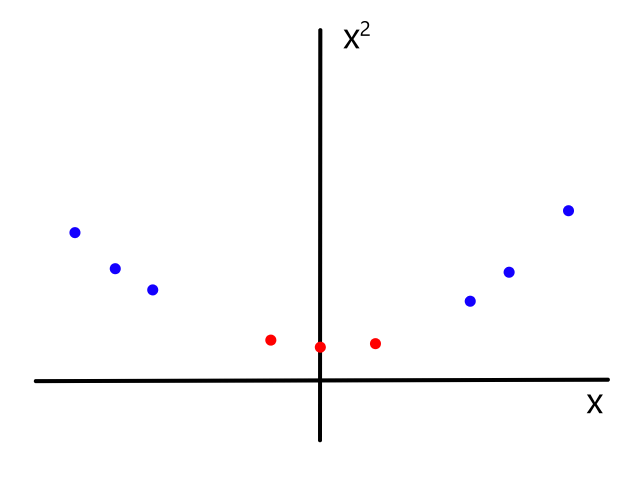

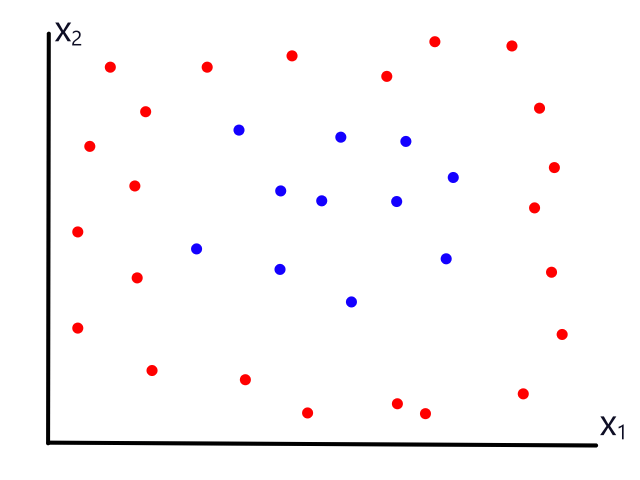

Polynomial Regression

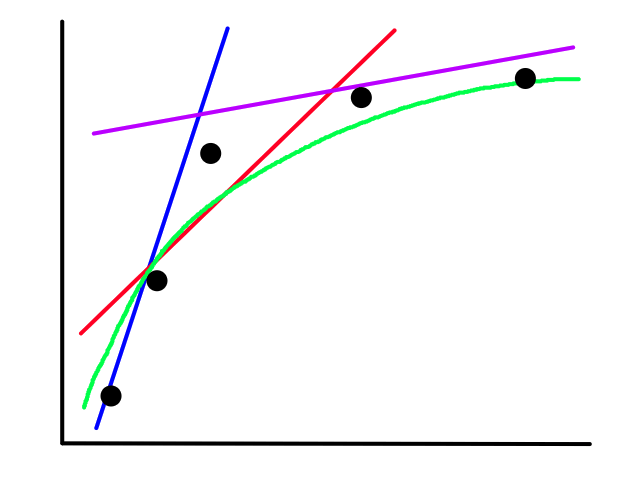

Sometimes using a line isn't the best fit for the data.

In this case, using a quadratic model would fit the data better.

The same can happen for classification.

This is usually the case because the output does not always have a linear relationship with the features.

Some examples:

Linear regression with one feature:

`h_theta(x)=theta_0+theta_1x`

Polynomial regression with one feature and order `2`:

`h_theta(x)=theta_0+theta_1x+theta_2x^2`

Logistic regression with two features:

`h_theta(x)=g(theta_0+theta_1x_1+theta_2x_2)`

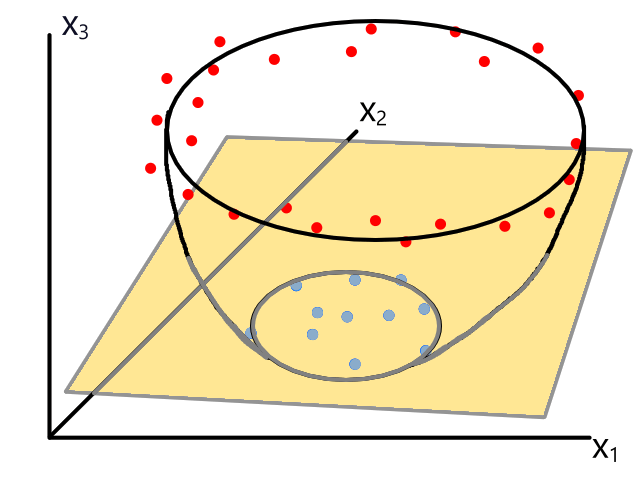

Polynomial classifier with two features and order `2`:

`h_theta(x)=g(theta_0+theta_1x_1+theta_2x_2+theta_3x_1^2+theta_4x_2^2+theta_5x_1x_2)`

Increasing the order of the model essentially involves adding a new feature to the dataset. If we have a feature `x`, we could multiply each value by itself and put the results in a new column to have `x^2`.

Training a polynomial model is no different than training a linear model. This is because we can encode a polynomial equation as a linear equation. For example, if we have `h_theta(x)=theta_0+theta_1x+theta_2x^2`, we can let `x_2=x^2` so that the new equation becomes:

`h_theta(x)=theta_0+theta_1x+theta_2x_2`

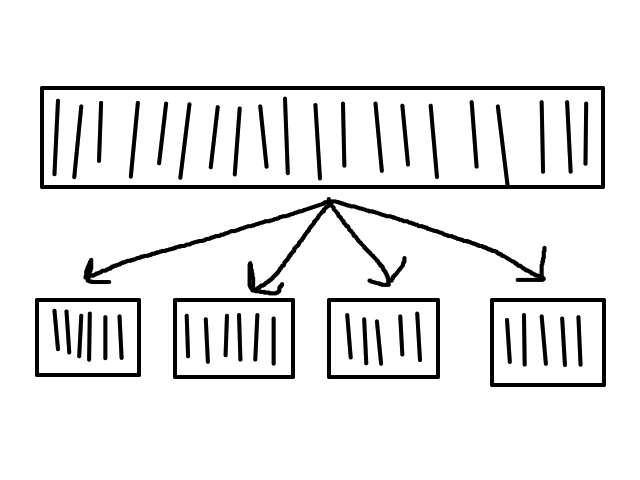

Random Forest

(See "A9) Ensemble Learning" for more background.)

Back to classification! More specifically, back to decision trees! But this time instead of just one tree, there's a whole forest of them. It's an ensemble learning method, so it builds several decision trees and combines their results to make a prediction. Having one big and deep tree usually leads to poor results (since it's usually the result of overfitting), so having many small trees prevents that. It's like having more people solving a problem rather than just one.

In order for all of the trees to work well together, each tree should be different from each other. So each tree will train on a different randomly-generated subset of the training dataset and on a different randomly-generated subset of features.

After each tree makes a prediction, the results are tallied up and the category with the most votes wins.

A random forest is not the same as a bunch of decision trees. A decision tree uses the whole dataset when training, while each decision tree in a random forest uses a subset of the dataset and features when training. All the trees in a bunch of decision trees will look the same (each node will have the same feature), so they will all make the same mistakes. On the other hand, in a random forest, each tree is different so if one tree makes a mistake, the other trees will likely not make the same mistake.

Let's say we had a random forest with two trees:

If we predict the fate of an adult female with a 2nd class ticket, the top/left tree would predict that the person did not survive. However, the bottom/right tree would predict that the person did survive. If I wasn't lazy enough to make a third three, the majority of the results would determine the final prediction of the random forest.

Advantages of Random Forest

- one of the most accurate classification algorithms

- very robust to noise and overfitting

- can handle big data with hundreds of features

- can handle missing values

K-Means Clustering

Up to this point, all the datasets we've been looking at have been labeled, i.e., each sample in the training dataset had a classification (e.g., rainy/sunny, survived/not survived) or a value (e.g., price). In some situations, the dataset will be unlabeled (see "A10) Unsupervised Learning" for more background), so it would be more helpful to put similar samples together in groups to see what we can learn from the groupings.

Let's say we had some unlabeled data plotted:

To start, we pick 2 random points (centroids) and group all the points that are closest to that point:

Then we find the center of those points for each group and make them the new centroids. Then we repeat the process until things no longer change.

So now we've divided the data into 2 clusters.

K-Means Clustering algorithm:

- Set `K` random points as initial centroids

- Assign each data sample to the cluster of the nearest centroid point

- Update centroid locations to the mean/average location of the members of the cluster

- Repeat until samples and centroids are stable

Pseudocode:

Let `x^((i))` be the data sample at index `i`. Let `c^((i))` be the index of the cluster to which `x^((i))` is assigned. Let `mu_k` be the centroid of cluster `k`.

(If `x^((1))` is in cluster 5, then `c^((1))=5`)

Randomly initialize `K` cluster centroids `mu_1, mu_2, ..., mu_k`

Cluster assignments: assign `c^((i))` the index of the cluster centroid closest to `x^((i))`, i.e., `c^((i))=min_k||x^((i))-mu_k||^2`

Move centroids: assign `mu_k` the average of points assigned to cluster `k`

Picking random points as the starting centroid can make the process of clustering too long if the random points happened to be far away from the data points. So the data points themselves are usually chosen as the initial centroids to make sure they are close to the data.

If we are lucky, then the results will be good:

But if we are unlucky, then the results will be bad:

So picking random points can lead to random results. The best way to deal with this is to repeat the whole thing several times and select the best clustering results. But what does "best" mean?

Another Cost Function

In this case, "best" means that the total average distance from each data point to its cluster centroid is minimized. Each point should be pretty close to its cluster centroid. We can define the cost function to be:

`J=1/msum_(i=1)^m||x^((i))-mu_(c^((i)))||^2`

where `mu_(c^((i)))` is the cluster centroid for `x^((i))`

So each time perform clustering, we calculate `J` and pick the clustering with the lowest `J`.

Divide and Cluster

Sometimes the data won't be so easily separable, but it would still be helpful to group the data into clusters. For product segmentation, it would be useful to categorize clothing into sizes, like small, medium, large:

Every Cluster Begins With K

In some situations, like product segmentation, we already know how many clusters we want to have. But for situations which we're not familiar with, the ideal number of clusters may vary depending on the situation. To see what the ideal value for `K` is, we could plot the number of clusters against the cost function to see the tradeoff.

In the orange case, there is not much reduction in error after 3 clusters, so we can apply the elbow rule and say 3 clusters is ideal.

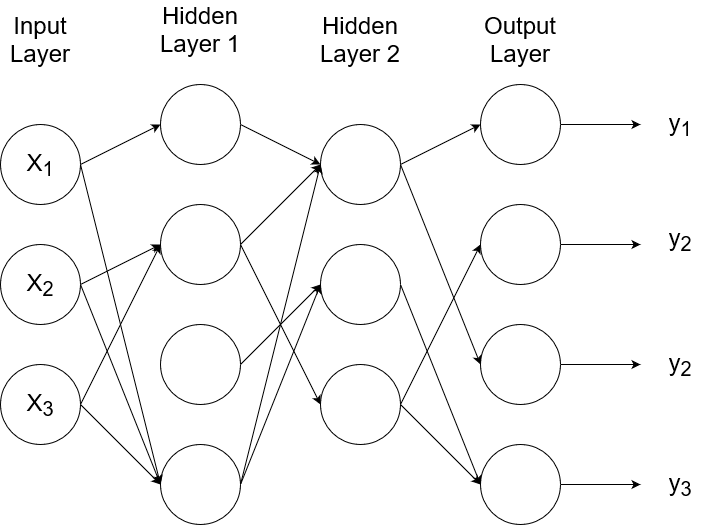

Artificial Neural Networks

Since we're training machines to learn from data, why not model them based on the best learning tool around? The human brain. Our brains are able to learn so many different things and respond to so many different inputs that it may seem impossible to try to replicate such a sophisticated system. Do we have to come up with different algorithms for each single thing the human body is capable of doing? After all, seeing an object and hearing sounds are completely different actions from each other, so why would a model that knows how to "see" necessarily know how to "hear"? Well, it turns out that only one general algorithm can be used to learn many different things.

In the 90s, some experiments were done on rats where scientists disconnected the nerves from the rats' ears to their auditory cortex (the part of the brain responsible for processing audio signals) and connected the nerves from their eyes to their auditory cortex instead. (So the part of the brain that "listens" no longer received sounds, but received light instead.) For the first few days, the rats couldn't see or hear anything. But over time, the rats started reacting to light, which meant that the auditory cortex had learned to see. The same results occurred for the somatosensory cortex (the part of the brain responsible for processing things we feel physically) which had also learned to see. This suggested that there is a general structure to the brain that can process different types of data and that learning was more about what type of data is provided.

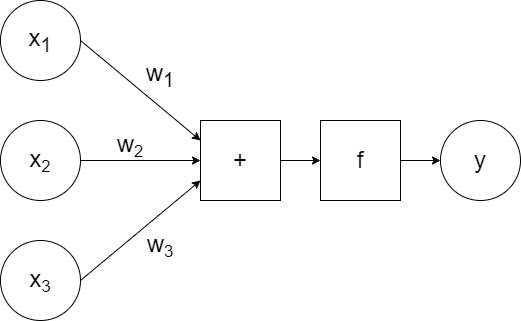

The way we try to mimic the brain is to try to simulate a neuron (nerve cell) and expand upon that to build a network of neurons. A neuron receives input through dendrites, processes the input in the nucleus, and transmits its output through axon terminals, which are connected to other neurons' dendrites. So the output of one neuron is the input to another neuron.

Artificially, it looks something like:

`x_1`, `x_2`, `x_3` are the inputs to the neuron, which are passed to the model along with the weights `w_1`, `w_2`, `w_3`. The model calculates the linear combination of the inputs (`w_1x_1+w_2x_2+w_3x_3`) and passes it to the activation function `f`, which generates some output `y`. (So `y=f(w_1x_1+w_2x_2+w_3x_3)`.)

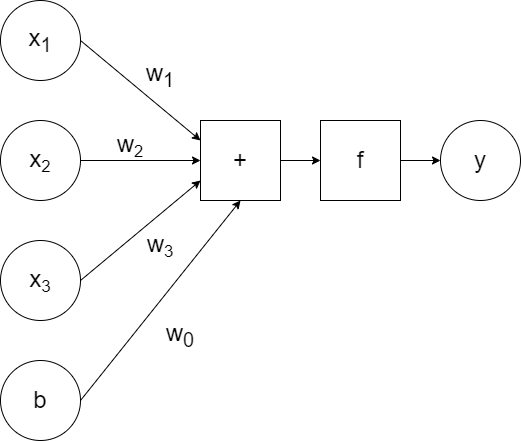

In addition to the weighted inputs, we can add another input that repesents bias.

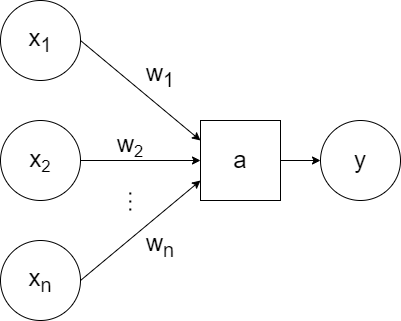

For simplicity, a generic `a` can be used to represent the activation function and the bias can be excluded visually (but included when training):

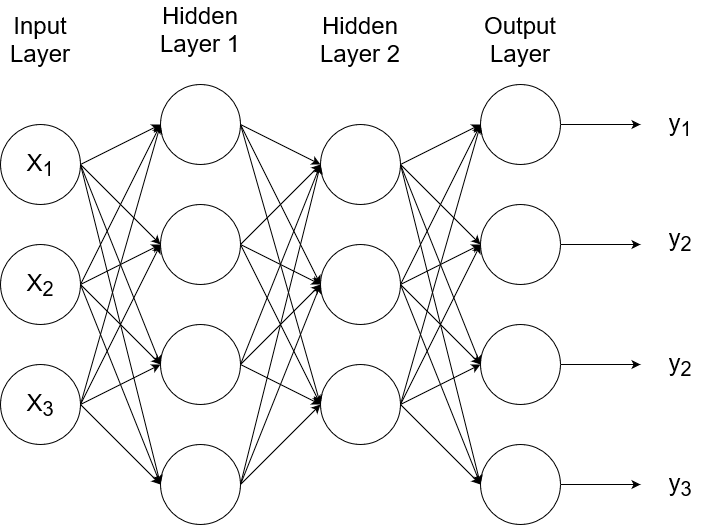

So that represents one neuron. A neural network consists of layers of neurons.

The input layer (also referred to as layer 0) receives and transfers the inputs without doing any computations on them. The last layer is called the output layer. All the layers in between are called the hidden layers. (In this example, there is only one hidden layer.) The connections from one node to another node are weighted connections, where the weight is represented by `w`. The notation reads:

`w_(ij)^((l))`

where `i` is the node it's going to, `j` is the node it's coming from, and `l` is the layer it's going to.

If we were to write out mathematically the value of each node, it would look like this:

`a_1^((1))=g(w_(10)^((1))b^((1))+w_(11)^((1))x_1+w_(12)^((1))x_2+w_(13)^((1))x_3)`

`a_2^((1))=g(w_(20)^((1))b^((1))+w_(21)^((1))x_1+w_(22)^((1))x_2+w_(23)^((1))x_3)`

`a_3^((1))=g(w_(30)^((1))b^((1))+w_(31)^((1))x_1+w_(32)^((1))x_2+w_(33)^((1))x_3)`

`y=a_1^((2))=g(w_(10)^((2))b^((2))+w_(11)^((2))a_1^((1))+w_(12)^((2))a_2^((1))+w_(13)^((2))a_3^((1)))`

assuming `g` is the activation function

And this is just a network with 1 hidden layer. It gets messy quickly, so representing things using vectors keeps things compact.

`bb a^((1))=[[a_1^((1))],[a_2^((1))],[a_3^((1))]]`

`bb W^((1))=[[w_(10)^((1)),w_(11)^((1)),w_(12)^((1)),w_(13)^((1))],[w_(20)^((1)),w_(21)^((1)),w_(22)^((1)),w_(23)^((1))],[w_(30)^((1)),w_(31)^((1)),w_(32)^((1)),w_(33)^((1))]]`

`bb x=[[b],[x_1],[x_2],[x_3]]`

So now the value of each node looks like this:

`bb a^((1))=g(bb W^((1))bb x)`

`y=bb a^((2))=g(bb W^((2))bb a^((1)))`

A neural network with one node in the output layer will output just one thing (e.g., rainy or sunny). But a network can have multiple nodes in the output layer.

This means the network will have multiple outputs. If we give a picture of a tree as input, the outputs can be whether the picture is of a tree or not, where the tree is, and the size of the tree. Or the outputs can be probabilities. If we have four possible types of outputs (e.g., cat, dog, horse, bird), each output can be the probability that it is each of those classes. So an output of `[[0.6],[0.4],[0],[0]]` would mean that there is a 60% chance that the image is of a cat and 40% chance that it is a dog.

You've Activated My Function!

The activation function should be nonlinear. (I believe using a linear function would be like making a line out of a line, i.e., there is no effect.) The simplest function to use is a step function.

Some popular choices include the logistic sigmoid function (yes, the same one back in logistic regression), the rectified linear unit (ReLU) function:

`RELU(x) = {(0 if x lt 0),(x if x >= 0):}`

and Softplus, which is the smooth approximation of ReLU:

`text(Softplus)(x) = log(1+e^x)`

Building Logical Operators

As a reminder, here's the sigmoid function:

Using this as the activation function (represented by `g`), we can simulate all of the binary operators, like logical not, and, or, nor, xor, etc.

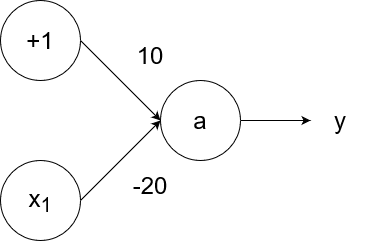

The negation (logical not) operator outputs 1 for an input of 0 and outputs 0 for an input of 1. We can simulate the negation operator with the following neural network:

So `y=g(10-20x_1)`.

- If `x_1=1`, then the output is `y=g(10-20*1)=g(10-20)=g(-10)=0`.

- If `x_1=0`, then the output is `y=g(10-20*0)=g(10-0)=g(10)=1`.

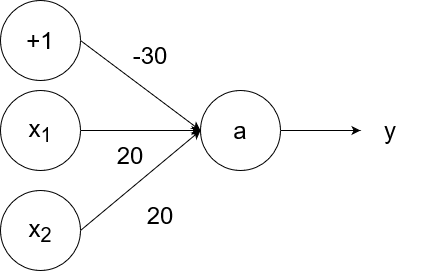

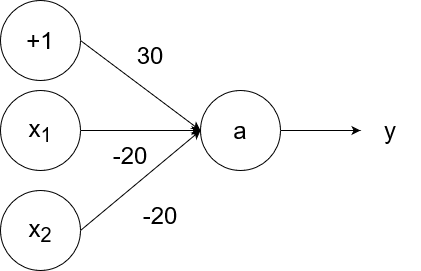

The logical and operator takes in two inputs. If both of them are 1, then the output is 1. If at least one of the inputs is 0, then the output is 0.

So `y=g(20x_1+20x_2-30)`.

- If `x_1=1` and `x_2=1`, then the output is `y=g(20*1+20*1-30)=g(40-30)=g(10)=1`.

- If `x_1=1` and `x_2=0`, then the output is `y=g(20*1+20*0-30)=g(20-30)=g(-10)=0`.

- If `x_1=0` and `x_2=1`, then the output is `y=g(20*0+20*1-30)=g(20-30)=g(-10)=0`.

- If `x_1=0` and `x_2=0`, then the output is `y=g(20*0+20*0-30)=g(0-30)=g(-30)=0`.

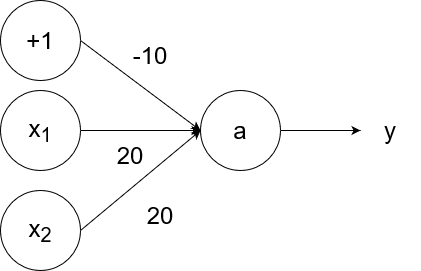

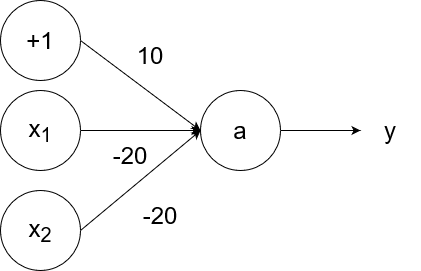

The logical or operator takes in two inputs. If both of them are 0, then the output is 0. If at least one of the inputs is 1, then the output is 1.

So `y=g(20x_1+20x_2-10)`.

- If `x_1=1` and `x_2=1`, then the output is `y=g(20*1+20*1-10)=g(40-10)=g(30)=1`.

- If `x_1=1` and `x_2=0`, then the output is `y=g(20*1+20*0-10)=g(20-10)=g(10)=1`.

- If `x_1=0` and `x_2=1`, then the output is `y=g(20*0+20*1-10)=g(20-10)=g(10)=1`.

- If `x_1=0` and `x_2=0`, then the output is `y=g(20*0+20*0-10)=g(0-10)=g(-10)=0`.

The logical nand (not and) operator takes in two inputs. If both of them are 1, then the output is 0. If at least one of the inputs is 0, then the output is 1.

So `y=g(-20x_1-20x_2+30)`.

- If `x_1=1` and `x_2=1`, then the output is `y=g(-20*1-20*1+30)=g(-40+30)=g(-10)=0`.

- If `x_1=1` and `x_2=0`, then the output is `y=g(-20*1-20*0+30)=g(-20+30)=g(10)=1`.

- If `x_1=0` and `x_2=1`, then the output is `y=g(-20*0-20*1+30)=g(-20+30)=g(10)=1`.

- If `x_1=0` and `x_2=0`, then the output is `y=g(-20*0-20*0+30)=g(0+30)=g(30)=1`.

The logical nor (not or) operator takes in two inputs. If both of them are 0, then the output is 1. If at least one of the inputs is 1, then the output is 0.

So `y=g(-20x_1-20x_2+10)`.

- If `x_1=1` and `x_2=1`, then the output is `y=g(-20*1-20*1+10)=g(-40+10)=g(-30)=0`.

- If `x_1=1` and `x_2=0`, then the output is `y=g(-20*1-20*0+10)=g(-20+10)=g(-10)=0`.

- If `x_1=0` and `x_2=1`, then the output is `y=g(-20*0-20*1+10)=g(-20+10)=g(-10)=0`.

- If `x_1=0` and `x_2=0`, then the output is `y=g(-20*0-20*0+10)=g(0+10)=g(10)=1`.

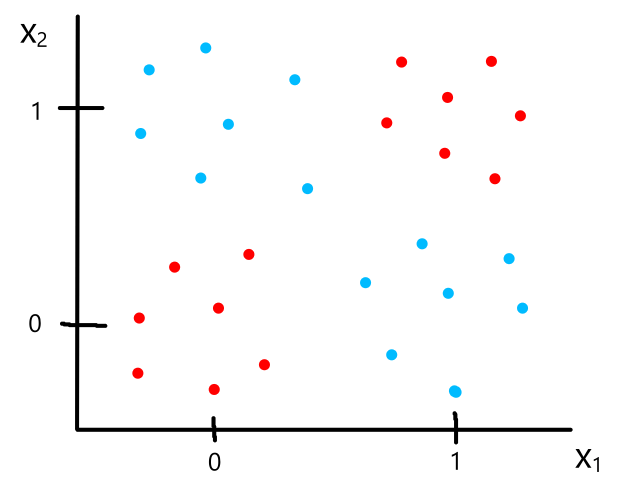

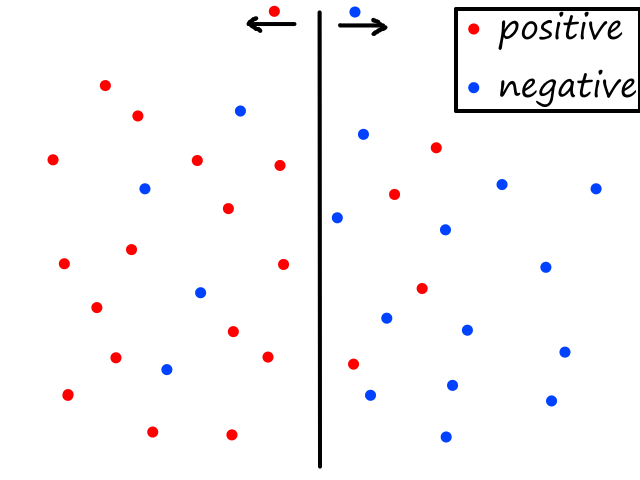

Being able to simulate logical operators can come in handy for some classification problems. Consider this dataset:

where we can interpret red being 1 and blue being 0.

It would be impossible to use a linear model to perform classification. It's possible to use a higher-order model, but it is much cleaner to use a logical operator in this case. Notice that when both inputs are the same number, then the output is 1. When both inputs are different numbers, then the output is 0. This is actually how the xnor (exclusive not or) operator works.

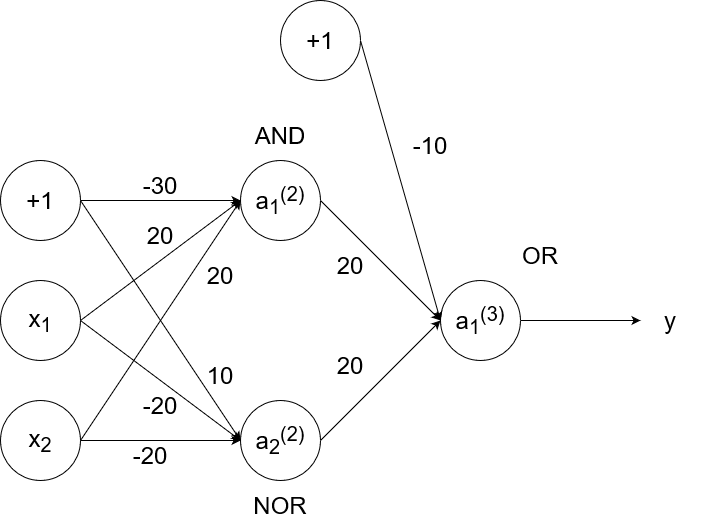

So `y=x_1text( XNOR )x_2`, which is equivalent to `(x_1text( AND )x_2)text( OR )(x_1text( NOR )x_2)`. We have the neural networks to simulate and, or, and nor already, so we can combine them to simulate xnor.

- If `x_1=1` and `x_2=1`, then `a_1^((2))=1`, `a_2^((2))=0`, and `a_1^((3))=y=1`.

- If `x_1=1` and `x_2=0`, then `a_1^((2))=0`, `a_2^((2))=0`, and `a_1^((3))=y=0`.

- If `x_1=0` and `x_2=1`, then `a_1^((2))=0`, `a_2^((2))=0`, and `a_1^((3))=y=0`.

- If `x_1=0` and `x_2=0`, then `a_1^((2))=0`, `a_2^((2))=1`, and `a_1^((3))=y=1`.

The Cost Function Is Back!

When a neural network is trained, it tries to find the best structure. This means it tries to find the best weights to use to connect each of the nodes. To determine what is "best", we need to bring back the cost function that represents the error and minimize the function.

The cost function for neural networks turns out to be very similar to the cost function for logistic regression. This is because neural networks can be seen as an advanced version of logistic regression.

If we look at just the output layer of a neural network, we can see that it receives some inputs multiplied by some weights. Using the sigmoid function as the activation function, this is the same as logistic regression where the inputs are the features and the weights are the `theta`s.

The inputs to logistic regression are the features themselves, while the inputs to the output layer of a neural network are the outputs from the previous layers, which aren't equal to the features at that point. In fact, the inputs to the output layer are new "features" that the neural network created to best learn and represent the data. So the hidden layers of a neural network can be seen as a feature learning process.

It's kind of like seeing a person with our eyes. The raw light that first reaches our eyes is like the input layer. Then as the light signals move through our brain, it processes them so that we see the silhouette of a person. Then they move on to the next layer so that we see a face. Then they move on to the final layer so that we recognize that the face belongs to our friend (or enemy if you roll that way).

The cost function for logistic regression is:

`J(bb theta)=-1/msum_(i=1)^m[y^((i))logh_theta(bb x^((i)))+(1-y^((i)))log(1-h_theta(bb x^((i))))]`

The cost function for neural networks is:

`J(bb W)=-1/msum_(i=1)^msum_(k=1)^K[y_k^((i))logh_W(bb x^((i)))_k+(1-y_k^((i)))log(1-h_W(bb x^((i))))_k]`

where `y^((i))` is the actual label for the `i^(th)` sample,

`h_W(x^((i)))` is the predicted label for the `i^(th)` sample,

`m` is the number of training samples,

`K` is the number of outputs

Overfitting can happen if the network is too complex. So we can add a regularization term to the cost function so that the weights are minimized as well:

`lambda/(2m)sum_(l=1)^(L-1)sum_(i=1)^(s_l)sum_(j=1)^(s_l+1)(w_(ij)^((l)))^2`

The result is usually that some of the weights get minimized to zero, which removes a connection between nodes. So a neural network could end up looking like this:

A neural network that is overfit is like a brain that overthinks. Having too many connections between neurons results in the brain being less effective and efficient, so the brain also does regularization to make it simpler. This is called synaptic pruning.

Backpropagation: I put my inputs, flip it and reverse it

When building a neural network, we decide how many layers and nodes per layer to use. The part that gets learned by the machine is what weights to use. Backpropagation is a systematic way to train a neural network so it can learn the weights.

In the beginning, we start with random weights. One training sample is used as input and the generated output (denoted as `o`) is compared with the actual output (denoted as `y`). Using the cost function, the error is calculated between the generated output and the actual output, and this error is propagated backwards through the network to update the weights. And then this process is repeated for all training samples.

For simplicity, we can assume that the cost function is `J=1/2(y-o)^2`. Also, we can assume that the activation function being used is the sigmoid function: `g(z)=1/(1+e^(-z))`. Then the gradient error would be

`delta=(partialJ)/(partialz)=(y-o)o(1-o)`

(the `o(1-o)` term comes from the derivative of the sigmoid function)

Then we use that gradient error to update the weights:

`w_(ij)^((l))(text(new))=w_(ij)^((l))(text(old))+alphadeltaa_i^((l-1))`

where `alpha` is the learning rate*

All of this was just for the output layer. To calculate the gradient error for the hidden layers, we use a different equation:

`delta_i^((l-1))=[sumw_(ji)^((l))delta_j^((l))]a_i^((l-1))(1-a_i^((l-1)))`

And to update the weights:

`w_(ij)^((l))(text(new))=w_(ij)^((l))(text(old))+alphadelta_i^((l))a_i^((l-1))`

*this learning rate is similar to the learning rate in gradient descent. In fact, backpropagation is a sort of different version of gradient descent (much like the output layer is a different version of logistic regression).

In gradient descent, we had this:

`theta_j = theta_j - alphadel/(deltheta_j)J(theta_0, theta_1)`

where that formula was used to take steps towards the minimum of the cost function `J`.

In backpropagation, we have this:

`w_(ij)^((l))(text(new))=w_(ij)^((l))(text(old))+alphadelta_i^((l))a_i^((l-1))`

It looks similar to taking steps, except we're tuning the weights. It's more like baking/cooking where we're adjusting how much of each ingredient is being added. We nudge the weights in the direction that minimizes error, so that's why we use the gradient error to update the weights.

Backpropagation can be seen as an implementation of the chain rule for derivatives. We can view each layer of a neural network as a function:

So the output would be:

`o=f(g(h(x)))`

Since we used random weights, there will be some error. For simplicity, let's use `(o-y)^2` to calculate error. If we want to minimize this error, then we take the derivative of it, which turns out to be:

`2(o-y)o'`

This means that in order to minimize error, we have to calculate the derivative of the output `o`. Since `o=f(g(h(x)))`, the derivative of `o` (by the chain rule) is:

`f'(g(h(x)))cdotg'(h(x))cdoth'(x)`

Well it turns out that when we calculate the gradient error and backpropagate it to the previous layers, it is similar to computing the derivative above.

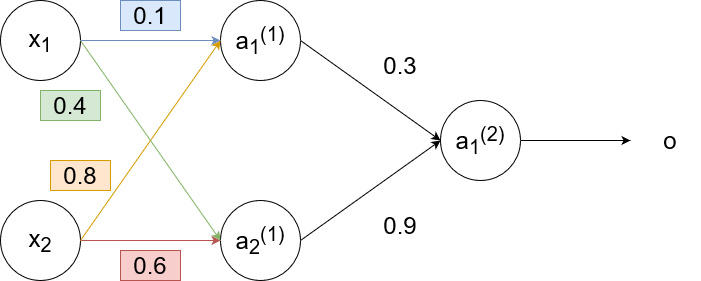

This is an example of backpropagation in action. We will use the sigmoid function `g(z)=1/(1+e^(-z))` as the activation function and use the learning rate `alpha=1`. Suppose we had this neural network with these weights: (biases excluded for simplicity)

For the training sample, suppose we have `x_1=0.35`, `x_2=0.9`, and `y=0.5`. Then

`a_1^((1))=g(w_(11)^((1))x_1+w_(12)^((1))x_2)=g(0.1cdot0.35+0.8cdot0.9)~~0.68`

`a_2^((1))=g(w_(21)^((1))x_1+w_(22)^((1))x_2)=g(0.6cdot0.9+0.4cdot0.35)~~0.6637`

`o=a_1^((2))=g(w_(11)^((2))a_1^((1))+w_(12)^((2))a_2^((1)))=g(0.3cdot0.68+0.9cdot0.6637)~~0.69`

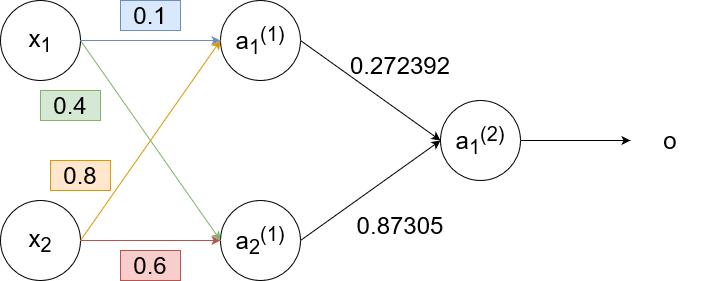

There is some error in the generated output (0.69) since the actual output should be 0.5. We calculate the gradient error to get:

`delta=(y-o)o(1-o)=(0.5-0.69)cdot0.69cdot(1-0.69)=-0.0406`

Now we backpropagate the error to the second layer. We update the weights using the gradient error:

`w_(11)^((2))(text(new))=w_(11)^((2))+alphadeltaa_1^((1))=0.3+1cdot-0.0406cdot0.68=0.272392`

`w_(12)^((2))(text(new))=w_(12)^((2))+alphadeltaa_2^((1))=0.9+1cdot-0.0406cdot0.6637=0.87305`

and calculate the gradient error to use for the next (previous? 🤔) layer:

`delta_1^((1))=[w_(11)^((2))delta]a_1^((1))(1-a_1^((1)))=[0.3cdot-0.0406]cdot0.68cdot(1-0.68)=-0.00265`

`delta_2^((1))=[w_(12)^((2))delta]a_2^((1))(1-a_2^((1)))=[0.9cdot-0.0406]cdot0.6637cdot(1-0.6637)=-0.00815`

So now the neural network looks like this:

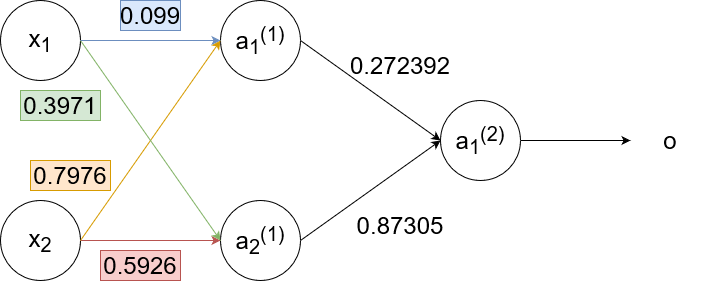

Now we backpropagate to the first layer:

`w_(11)^((1))(text(new))=w_(11)^((1))+alphadelta_1^((1))x_1=0.1+1cdot-0.00265cdot0.35=0.099`

`w_(12)^((1))(text(new))=w_(12)^((1))+alphadelta_1^((1))x_2=0.8+1cdot-0.00265cdot0.9=0.7976`

`w_(21)^((1))(text(new))=w_(21)^((1))+alphadelta_2^((1))x_1=0.4+1cdot-0.00815cdot0.35=0.3971`

`w_(22)^((1))(text(new))=w_(22)^((1))+alphadelta_2^((1))x_2=0.6+1cdot-0.00815cdot0.9=0.5926`

So the neural network finally looks like this:

Notice how `delta_1^((1))` and `delta_2^((1))` are smaller than `delta`. The further we backpropagate, the smaller the `delta`s become, which results in the weights staying pretty much the same. This effect is called the "vanishing gradient".

Deep Learning

The very simple explanation of deep learning is that it is a wide and deep neural network, meaning that it has many many neurons and layers. While deep learning does use neural networks, the main characteristic of deep learning is that it tries to learn what features are important, instead of us giving the neural network the features. Sometimes, the features that the network learns are better than the features we provide to it. And in some cases, it can be time expensive to create the features ourselves (e.g., for unsupervised learning).

Because the neural network is often wide and deep, there are a lot of weights for it to learn, so it needs a lot of data to train with. In fact, deep learning generally outperforms other machine learning algorithms only when the dataset is large enough.

Vanishing Gradient: Do You See It? Now You Don't

Neural networks are trained using backpropagation, which is the process of calculating the error and using that calculation to update the weights in each layer. The issue with backpropagation is that usually the `delta`s are very very small, which results in very very little impact on the weights. Furthermore, the `delta`s get smaller as backpropagation continues, so the first few layers remain virtually unchanged. The first few layers are important because their outputs are used for the rest of the layers, so the first few layers need to be on point. This problem is greatly exacerbated by the fact that deep learning uses wide and deep neural networks.

Activation Function

The `delta`s are determined by the activation function, so using a different activation function could help. The sigmoid function is not that great of a function to use because it returns a value between 0 and 1. Multiplying a weight by a number between 0 and 1 isn't going to change it much. A better function to use is ReLU, since it returns a value greater than 1.

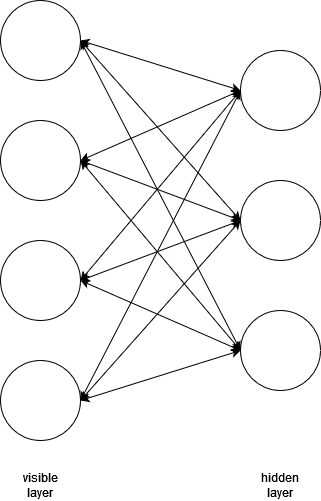

Restricted Boltzmann Machines

Another way to solve the vanishing gradient problem is to use a different type of structure that isn't so wide and deep. RBM only uses two layers, but they are bidirectional, meaning they pass their inputs and outputs back and forth to each other. The first layer is the "visible layer" and the second layer is the "hidden layer".

The inputs are passed through the layers, which will produce some output. The output is then fed backwards through the network to try and reproduce the original input as close as possible. After repeating this process several times, the network will learn what the best weights are to represent the input data.

Deep Belief Networks

So an RBM can optimize a pair of layers. What if we apply this RBM idea to every layer in a deep neural network? Would that mean that we would have optimized layers? Yes, actually. A deep belief network (DBN) is a deep neural network where its layers are RBMs.

Instead of starting with random weights, we are now starting with optimized weights. So backpropagation will be much faster.

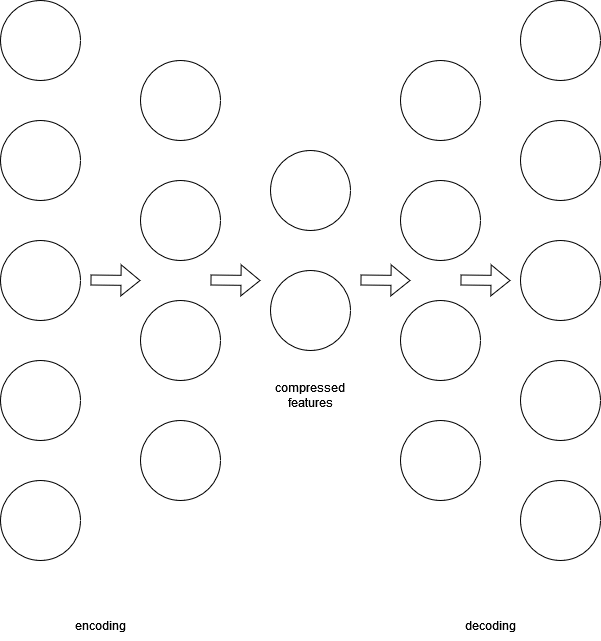

Deep Autoencoder

#dimensionalityreduction

We can combine RBMs to get a DBN. We can also combine DBNs to get a deep autoencoder. A deep autoencoder is an unsupervised deep neural network that is useful for extracting the most important part of data. It is made up of two DBNs: one used for encoding data and the other used for decoding data. The encoding network learns the best way to compress the input and the decoding network is used to reconstruct the data. Minimizing the difference between the original input data and the reconstruction results in a network that knows how to compress the data in the best way without significant data loss.

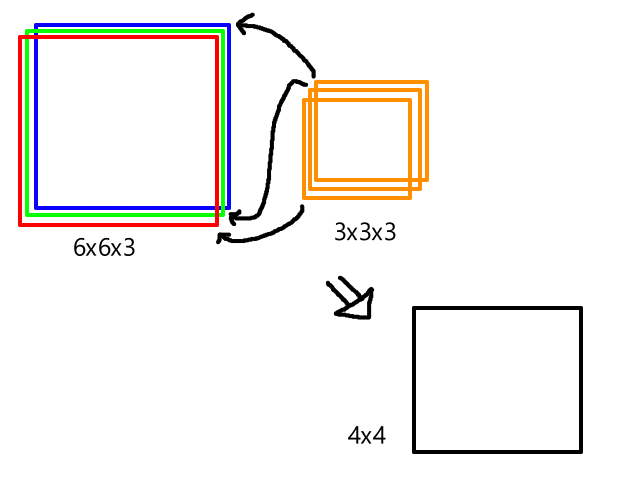

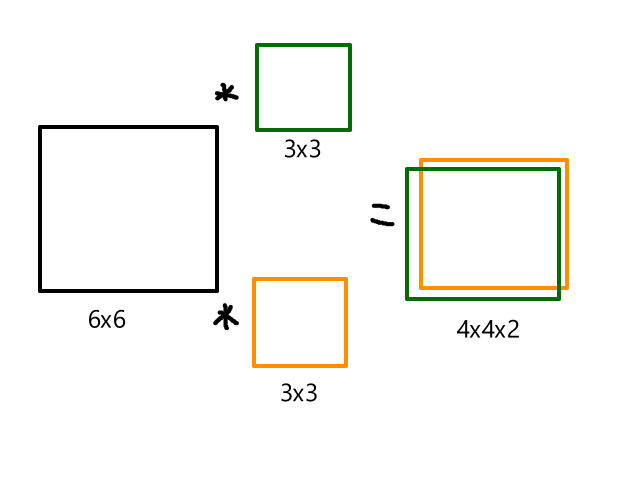

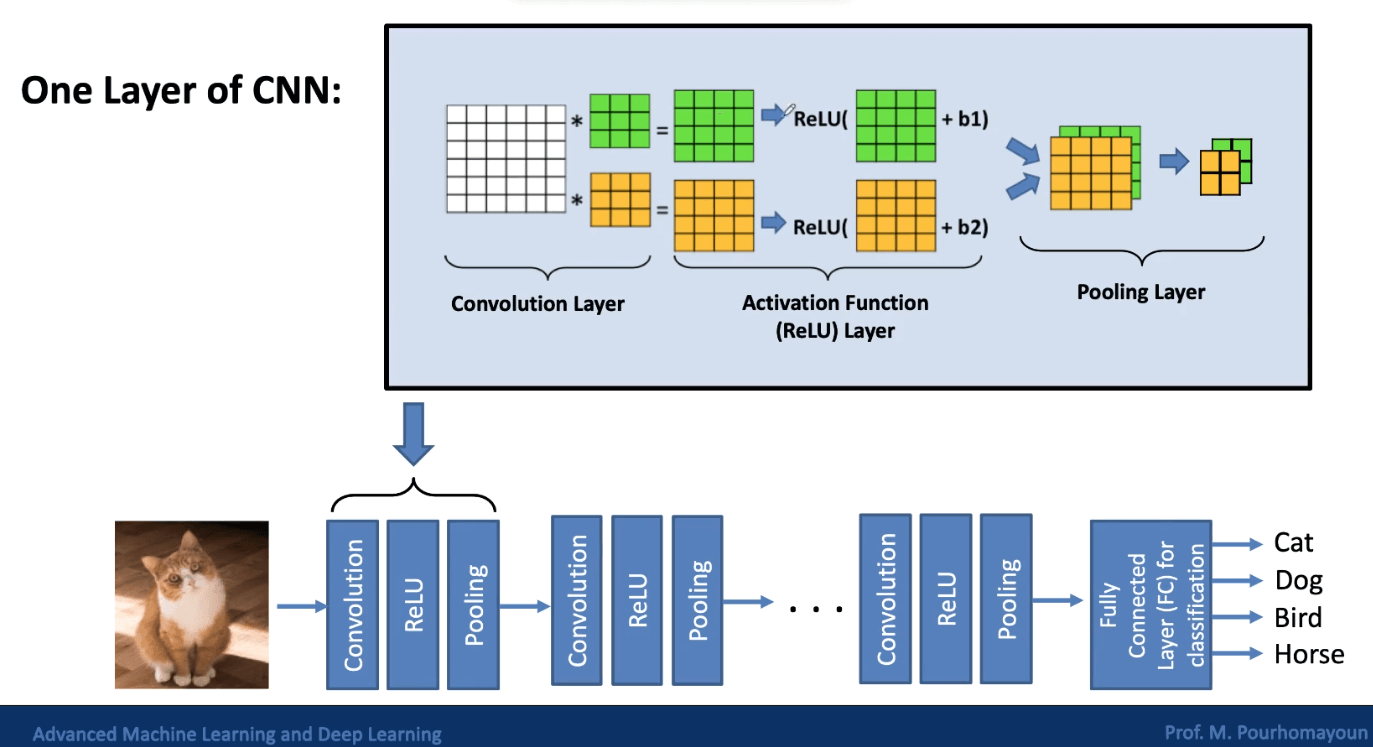

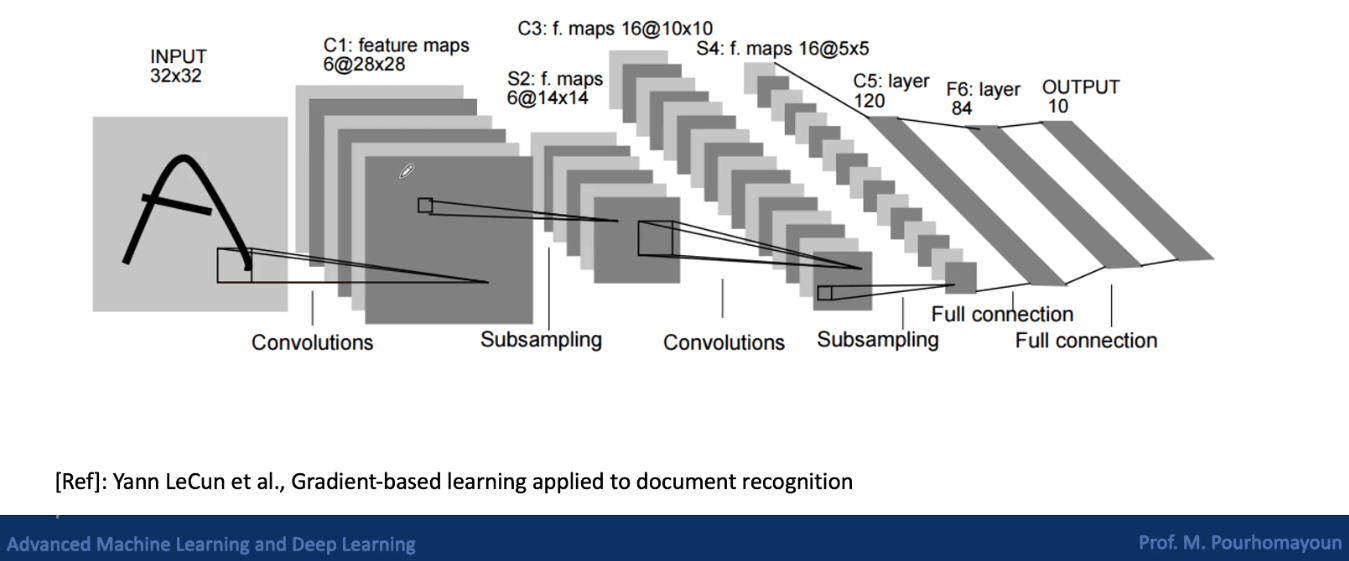

Convolutional Neural Networks

Convolutional neural networks are a type of deep neural network that is commonly used for image classification and object recognition. Regular neural networks don’t work well with images because images have high dimensionality. Each pixel is considered a feature, so an image that is 100 x 100 pixels already has 30,000 features. This means that there are at least 30,000 weights to train in the first layer, which is not ideal.

CNNs are designed to reduce dimensionality by extracting patterns from images, so that all the pixels don’t need to be processed. Some of the layers in a CNN are called convolutional layers, which are used for feature extraction. There are also pooling layers, which are used for dimensionality reduction.

Edge Detection

In order to identify objects in images, we need to be able to detect edges. Convolution is a process that allows us to do this. In convolution, a filter (a.k.a. kernel) is applied to each pixel of the image. Applying the filter puts a weight on each pixel, and these weights are used to determine whether there is an edge at that pixel or not.

Let's suppose we have this image:

| 1 | 1 | 1 | 0 | 0 |

| 0 | 1 | 1 | 1 | 0 |

| 0 | 0 | 1 | 1 | 1 |

| 0 | 0 | 1 | 1 | 0 |

| 0 | 1 | 1 | 0 | 0 |

and this filter:

| 1 | 0 | 1 |

| 0 | 1 | 0 |

| 1 | 0 | 1 |

In the first step of convolution, we start with the top-left pixels. Applying the filter means multiplying each pixel by the corresponding square in the filter:

| 1*1 | 1*0 | 1*1 | 0 | 0 |

| 0*0 | 1*1 | 1*0 | 1 | 0 |

| 0*1 | 0*0 | 1*1 | 1 | 1 |

| 0 | 0 | 1 | 1 | 0 |

| 0 | 1 | 1 | 0 | 0 |

And then adding the products together:

`1xx1+1xx0+1xx1+0xx0+1xx1+1xx0+0xx1+0xx0+1xx1=4`

| 4 | ||

Then we move the filter over to the next set of pixels and repeat the same process:

| 1 | 1*1 | 1*0 | 0*1 | 0 |

| 0 | 1*0 | 1*1 | 1*0 | 0 |

| 0 | 0*1 | 1*0 | 1*1 | 1 |

| 0 | 0 | 1 | 1 | 0 |

| 0 | 1 | 1 | 0 | 0 |

`1xx1+1xx0+0xx1+1xx0+1xx1+1xx0+0xx1+1xx0+1xx1=3`

| 4 | 3 | |

After applying the filter to the whole image, we get the convolved image:

| 4 | 3 | 4 |

| 2 | 4 | 3 |

| 2 | 3 | 4 |

The example above was just some random filter, but using a specific filter allows us to detect edges. Consider this black and white image which has an edge right down the middle:

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

And this filter:

| 1 | 0 | -1 |

| 1 | 0 | -1 |

| 1 | 0 | -1 |

For the first step of convolution:

| 5*1 | 5*0 | 5*-1 | 5 | 0 | 0 | 0 | 0 |

| 5*1 | 5*0 | 5*-1 | 5 | 0 | 0 | 0 | 0 |

| 5*1 | 5*0 | 5*-1 | 5 | 0 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

The result is:

| 0 | |||||

The second step of convolution will be the same since the pixel values are the exact same.

| 0 | 0 | ||||

For the third step of convolution:

| 5 | 5 | 5*1 | 5*0 | 0*-1 | 0 | 0 | 0 |

| 5 | 5 | 5*1 | 5*0 | 0*-1 | 0 | 0 | 0 |

| 5 | 5 | 5*1 | 5*0 | 0*-1 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

| 5 | 5 | 5 | 5 | 0 | 0 | 0 | 0 |

The result is:

| 0 | 0 | 15 | |||

In the end, we will have this result:

| 0 | 0 | 15 | 15 | 0 | 0 |

| 0 | 0 | 15 | 15 | 0 | 0 |

| 0 | 0 | 15 | 15 | 0 | 0 |

| 0 | 0 | 15 | 15 | 0 | 0 |

Notice how the nonzero values are right down the middle, exactly where the edge was at in the original image.

There are many different types of filters that can detect different types of edges. Here are a few:

| 1 | 0 | -1 |

| 1 | 0 | -1 |

| 1 | 0 | -1 |

Vertical Edge Filter

| 1 | 1 | 1 |

| 0 | 0 | 0 |

| -1 | -1 | -1 |

Horizontal Edge Filter

| 0 | 1 | 0 |

| 1 | 0 | -1 |

| 0 | -1 | 0 |

Diagonal Edge Filter (top right to bottom left)

| 0 | 1 | 0 |

| -1 | 0 | 1 |

| 0 | -1 | 0 |

Diagonal Edge Filter (top left to bottom right)

We don't manually choose which filters to apply. We let the neural network learn what the most important edges are and it will automatically come up with the best set of filters to detect those edges. The values for the filters can be thought of as weights of a neural network that are learned.